Datadog Falls After Bernstein Downgrade: What a $226 Target Below the Stock Means for Investors

Key Stats for Datadog Stock

- Current Price: $248.30

- Target Price (Mid): ~$407

- Street Target: ~$244

- Potential Total Return: ~56%

- Annualized IRR: ~11% / year

- Max Drawdown: 48.62% (February 23, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

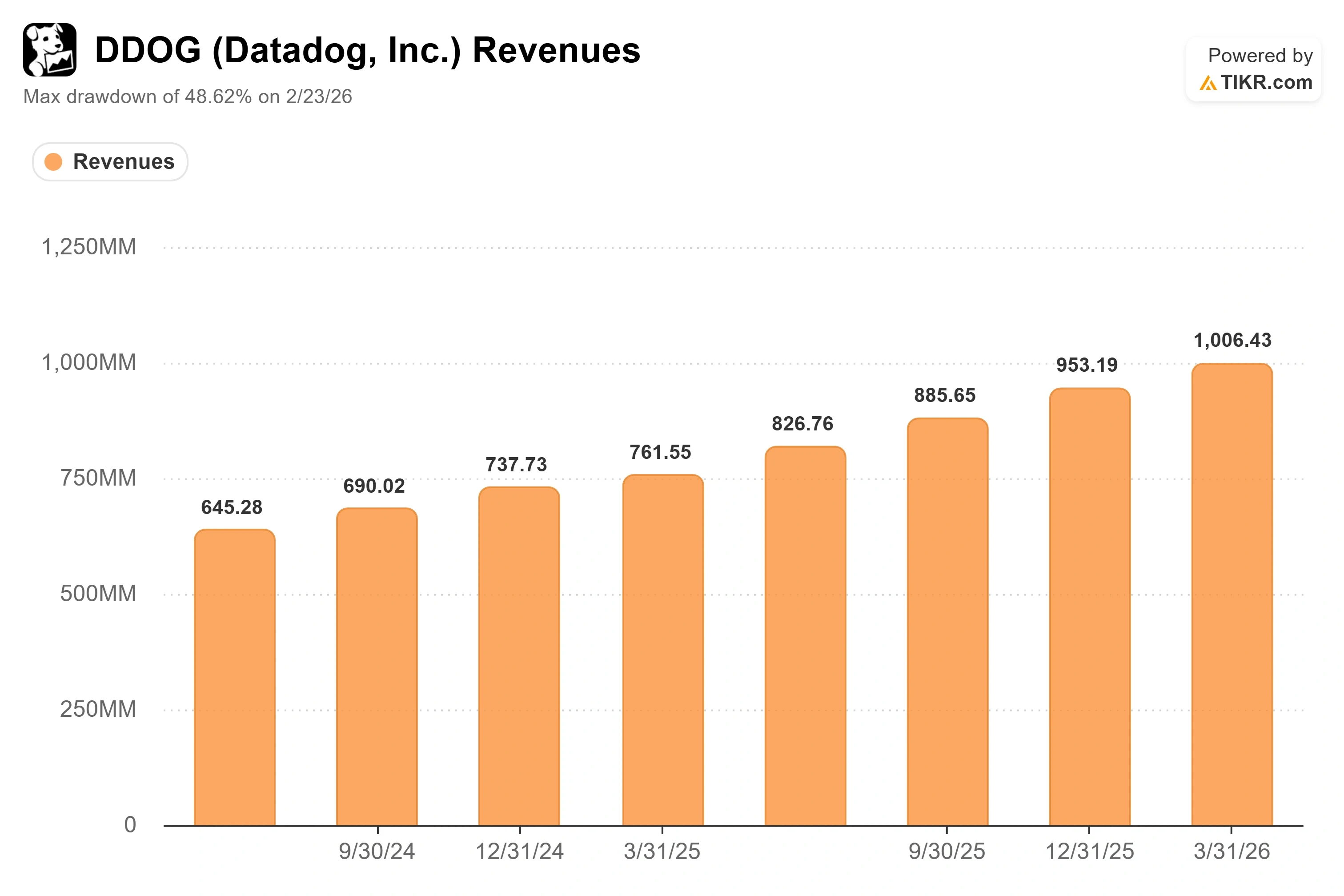

Datadog (DDOG) spent the first half of 2026 as one of software’s clearest winners, and on Monday, one of its supporters stepped off the train. Bernstein’s Peter Weed cut the stock to Market Perform from Outperform before the open on July 6, and shares fell about 4.6% to $248.30 in early trading. The move stung because it broke a run: DDOG had returned roughly 119% over the prior 90 days and sat near the top of its 52-week range.

Here is what makes the call worth a second look. Weed did not slash his price target. He raised it to $226 from $180 while downgrading the rating. That is an analyst conceding the business is worth more than he thought, then arguing the stock has still run past it. His new target sits below where DDOG trades, which tells you the disagreement is not about whether Datadog is a good company. It is about whether the next few quarters can clear a bar that the market has already raised.

A downgrade and a Street-high target in the same week

The timing sharpens the tension. Just days earlier, on July 2, Benchmark’s Yi Fu Lee lifted his DDOG target to a Street-high $330 from $260 and kept a Buy, citing customer and partner checks he called “excellent.” So within a single week, one respected shop called the stock a Buy at $330 and another pulled its Buy at $226. That spread, more than $100 wide, is the real story. The consensus that carried DDOG up all spring is fracturing, and investors are left holding two credible views of the same company.

Bernstein’s worry is specific, not vague. Weed argued that demand signals are slowing in both the enterprise segment and some AI Lab customers, and that the non-AI portion of the business, which he pegs at roughly 85% of revenue, could see its growth rate peak in the third quarter before hitting tougher year-over-year comparisons in Q4. Datadog’s Q1 report drew a positive reaction, with the stock rising 6.06% on May 7, so the market clearly rewards upside here. The question Bernstein raises is whether that upside is getting harder to deliver.

Datadog Revenues (TIKR)

Datadog Revenues (TIKR)

See historical and forward estimates for Datadog stock (It’s free!) >>>

What management said about the exact fear Bernstein is raising

This is where Datadog’s own words matter, because CFO David Obstler addressed the durability question directly at the Bank of America 2026 Global Technology Conference on June 3, weeks before the downgrade. Asked what gives the company confidence that growth continues, he made the case that the trend is structural, not a passing cycle.

“You have 70% plus of workloads that aren’t in the cloud. So we believe this has very long legs,” David Obstler, Chief Financial Officer, said at the conference. The point matters because Bernstein’s thesis is essentially a timing call on a demand plateau, and Obstler is arguing the runway is measured in decades of cloud migration, not quarters. He was candid that the path will not be a straight line, noting the business is consumption-based and will have “periods of investment” and “periods of optimization.” That honesty cuts both ways: it concedes the lumpiness Bernstein is flagging while insisting the direction is not in doubt.

Obstler also pushed back on the idea that AI is the whole story. He described a “confluence” of drivers behind the company’s large-enterprise wins, pointing to legacy companies with only “25%, 30% of workloads in the cloud right now” that are still early in modernizing. If that broad base of non-AI migration keeps compounding, the 85%-of-revenue cohort Bernstein is worried about looks less like a peak and more like a long grind higher.

Where Datadog’s valuation actually sits versus peers

None of this resolves the valuation question, and it is a fair one. On the TIKR Competitors data, Datadog trades at around 19.6x forward total enterprise value to revenues, well above the peer-group mean of about 11.4x. CrowdStrike sits at around 31x on the same measure and Palo Alto Networks at around 21x, while Fortinet trades near 14x. Datadog’s premium is real, but it is not the outlier in its cohort, and it is paired with faster revenue growth than most of the group. The premium is defensible so long as growth stays in the mid-20s. It becomes a problem the moment growth slips toward the peer average, which is precisely the risk Bernstein is pricing.

That is the tension in one sentence: a platform compounding faster than its peers, carrying a multiple that only works if the compounding holds. The bear does not need the business to break. It only needs growth to normalize a little faster than bulls expect, and the valuation multiples do the rest of the damage. The bull needs the non-AI base to keep defying gravity and the AI-native cohort to keep scaling, which is exactly what the last four quarters delivered.

Datadog NTM EV/Revenues (TIKR)

Datadog NTM EV/Revenues (TIKR)

See how Datadog performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $248.30

- Target Price (Mid): ~$407

- Potential Total Return: ~56%

- Annualized IRR: ~11% / year

Datadog Advanced Valuation Model (TIKR)

Datadog Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Datadog stock (It’s free!) >>>

The mid case rests on around 21% revenue CAGR and a net income margin expanding toward about 21%. The two revenue drivers are continued cloud-migration adoption across non-AI enterprises, Obstler’s “long legs” argument, and rising AI-native workload consumption as GPU training and inference customers scale. The margin driver is operating leverage on a business already near 80% gross margin, as the go-to-market and R&D investments season. The primary risk is the one Bernstein named: a faster-than-expected deceleration in the non-AI base that compresses the multiple before earnings catch up.

The upside case: growth holds in the mid-20s, the premium is validated, and the stock compounds toward the model’s target.

The downside case: growth normalizes toward the peer average, the multiple resets, and the stock stalls near Bernstein’s $226 regardless of solid fundamentals.

Conclusion

The debate now has a scoreboard, and it is the next earnings report. Bernstein’s entire thesis rests on non-AI growth peaking in Q3 and rolling over into Q4. That print is the first real test. Watch one number: broad-based revenue growth excluding the largest AI-native customer. If it holds in the mid-20s, Bernstein’s peak call looks early, and the bulls at $330 look right. If it slips toward 20% or below, the downgrade ages well, and the $226 target stops looking conservative. Everything else, the acquisitions, the DASH product launches, the AI headlines, is noise until that one figure lands.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Datadog?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Datadog, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Datadog alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Datadog on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Trump tells Netanyahu, ‘You’re f—ing crazy’ and Wall Street sees it as a sign he’s losing patience with the war and wants it done

Biden's Illegal Alien Invasion Sparked 30% Home Price Growth, 20% Rent Growth: Fed Paper

SPARC AI Overwatch Platform Demonstrates Long-Range Maritime Targeting in Major Test