Broadcom Just Got Downgraded by a Major Bank to a $437 Target. Is the Bear Case Right?

Key Stats for Broadcom Stock

- Current Price: $392.13

- Target Price (Mid): ~$1,090

- Street Target: ~$524

- Potential Total Return: ~178%

- Annualized IRR: ~26% / year

- Earnings Reaction: (12.59%) on June 3, 2026

- Max Drawdown: 28.95% on March 30, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

A Downgrade That Put a Number on the Fear

Broadcom (AVGO) just handed the market a bear case with a name attached. One day after record results, Macquarie cut Broadcom to Neutral and lowered its target to $437 from $513. The reason was not the quarter. It was the customer. The firm argued that Google, Broadcom’s largest AI buyer, is bringing MediaTek into its chip supply chain, and that Broadcom’s share of Google’s tensor processing unit (the custom AI chip Google designs with Broadcom) revenue could fall from roughly 95% in 2026 to 65% by 2028.

That call hit a stock already sliding. Broadcom closed at $392.13 on June 22, down 4.67% on the day, after a 12.59% drop on its June 3 earnings reaction and a peak-to-trough drawdown of almost 29% earlier this year. Bulls see demand that management calls insatiable. Bears see a concentration risk finally cracking open. The market cannot yet settle it, because the proof sits in deliveries that have not happened.

The Quarter Was Not the Problem

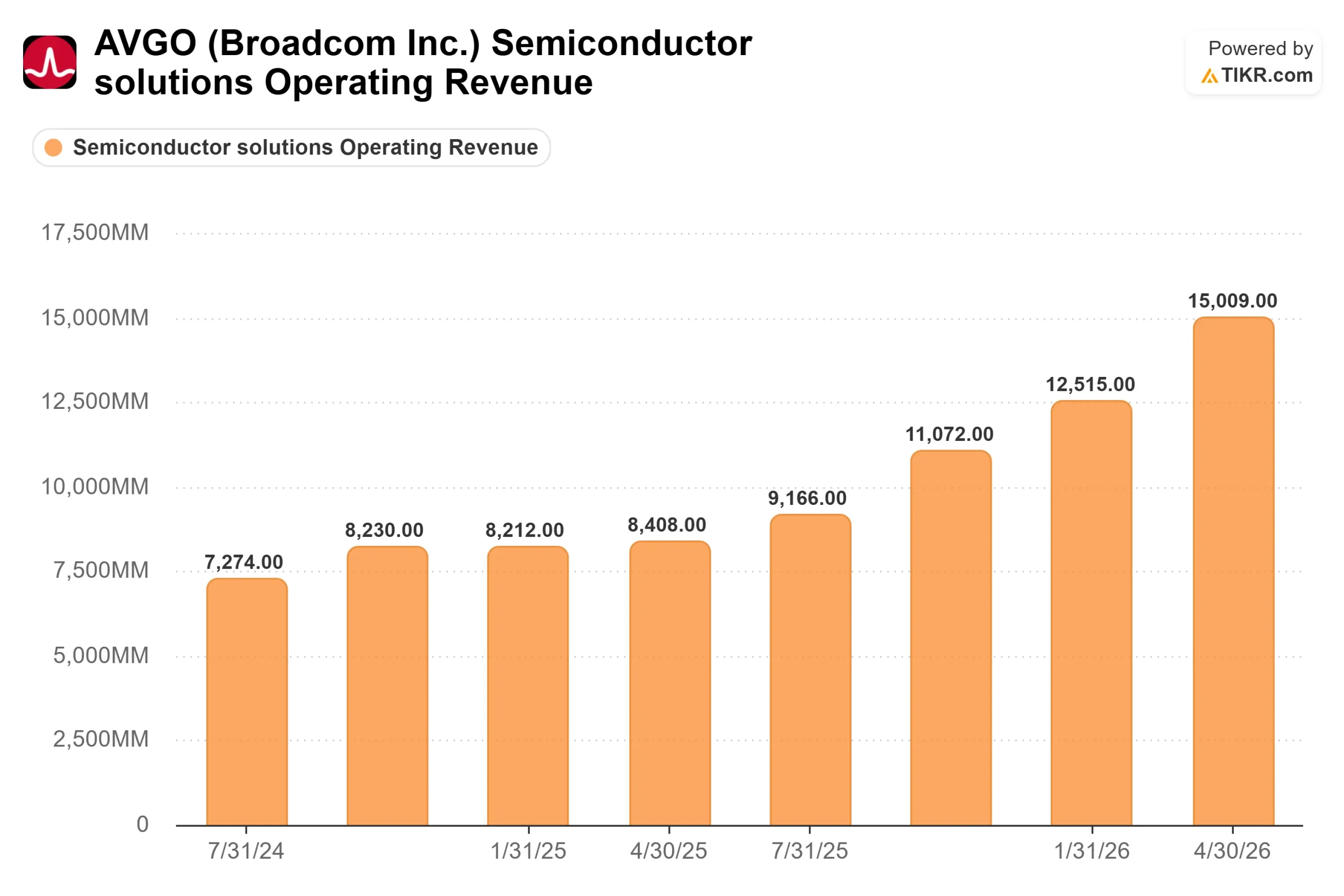

The fiscal Q2 results were exceptional. Revenue hit a record $22.19 billion, up 48% year over year and beating the $22.08 billion consensus. Adjusted earnings per share of $2.44 topped the $2.40 estimate. AI semiconductor revenue reached $10.8 billion, up 143%, and free cash flow crossed $10 billion in a single quarter for the first time.

So why the selloff? Guidance was strong, not raised. CEO Hock Tan held the full-year AI chip target at $56 billion instead of lifting it, and on a premium stock, steady reads as soft. The VMware software unit added pressure: revenue of $7.2 billion grew 9% with annual recurring revenue up 17%, but landed shy of estimates.

None of that signals a broken business. The bookings argue the opposite. Tan said AI bookings exceeded $30 billion in the quarter against $10.8 billion shipped, with visibility now running into 2028. The fear is not demand. The fear is who captures it.

Broadcom Semiconductor Solutions Operating Revenue (TIKR)

Broadcom Semiconductor Solutions Operating Revenue (TIKR)

See historical and forward estimates for Broadcom stock (It’s free!) >>>

The Google Question, in Tan’s Own Words

Macquarie’s case rests on one relationship, so what management said about it matters most. Pressed on the new Google agreement, Tan did not deny diversification. He framed it as a function of scale: he “fully expect[s] that there will be some diversity of sources” for Google as its AI compute consumption grows. That is the admission the bears seized on. Broadcom expects to share Google’s TPU business. The dispute is only about how much.

This is why both sides can be partly right. Macquarie raised its 2026 and 2027 earnings estimates even as it cut 2028, so the fight is about the back end, not next year. Tan’s counter is that the pie is growing faster than his slice is shrinking. Broadcom now has six core custom-chip customers, including Anthropic, OpenAI, Meta, and Google, with multi-gigawatt commitments through 2028. If total demand compounds faster than Broadcom’s share erodes, revenue still climbs.

One quieter shift fed the reset: Tan confirmed Broadcom will sell “chips only” rather than the complete integrated AI systems it had previously signaled. That trims the revenue per deal. It is a strategy change, not a demand problem.

Broadcom NTM EV/EBITDA (TIKR)

Broadcom NTM EV/EBITDA (TIKR)

What the Numbers Say After the Drop

Even Macquarie conceded downside looks limited by valuation, and the stock is now near the $400 level, which the firm called attractive. Broadcom trades at about 25 times next-twelve-month earnings and roughly 20 times forward EV/EBITDA, well below the mid-30s multiple it carried last autumn. The scary-looking 65 times trailing P/E spans quarters that predate the AI surge.

The peer screen frames the discount. On forward EV/EBITDA, Broadcom sits near 20x against a semiconductor peer median of around 28x, with AMD at 54x. Only NVIDIA screens are cheaper at about 17x, and it lacks Broadcom’s 93% software gross margins. For a company growing revenue 48% with a high-margin recurring software base, a below-median multiple is the discount the bears must justify.

The risk is real, not abstract. If Google’s shift to MediaTek moves faster than Tan implies, or if any anchor customer defers deployments, the second-half ramp the model depends on slips, and a premium stock with a 0.7% dividend yield has little cushion. That is the true bear case, and it is a 2028 question the data cannot answer yet. The counterweight is $30 billion in quarterly bookings and visibility into 2028, more forward certainty than almost any chip peer can claim.

See how Broadcom performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $392.13

- Target Price (Mid): ~$1,090

- Potential Total Return: ~178%

- Annualized IRR: ~26% / year

Broadcom Advanced Valuation Model (TIKR)

Broadcom Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Broadcom stock (It’s free!) >>>

TIKR’s mid-case scenario values Broadcom near $1,090 by October 2030, roughly 178% total return from $392.13, or about 26% a year over 4.4 years. Two revenue growth drivers carry it: the AI chip ramp, where bookings far outpace shipments, and the VMware subscription transition, completing in late 2026. The case assumes around 29% revenue growth and net income margins near 55%.

The margin driver is mix and operating leverage, with 90%-plus software gross margins offsetting lower-margin custom silicon while costs stay roughly flat. The primary risk is the one Macquarie named: losing Google TPU share faster than expected. Upside: if the six-customer backlog converts on schedule, the high case points toward roughly $3,365. Downside: faster share loss and multiple compression could drag the stock back toward the bear’s $437 zone.

Conclusion

The downgrade turned a vague worry into a testable claim, and the test has a date. Management guided fiscal Q3 AI chip revenue to $16 billion, up more than 200% year over year, the steepest bar Broadcom has ever set. Hit it, and the share-loss story looks premature against rising absolute dollars. Miss it on a premium stock, and Macquarie’s thesis gets its first real evidence. Watch the $16 billion AI line and any Google-delivery commentary when Broadcom reports after the close on September 3, 2026. That number settles the argument, not the next analyst note.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Broadcom?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Broadcom, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Broadcom alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Broadcom on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

NeoRiseWay.com Reviews: A Helpful Look at Modern Financial Opportunities for Investors

Ripple settled a tokenized Treasury with JPMorgan. What it means for XRP

Japanese Tech Giant’s Ambitious Bitcoin Accumulation