Coherent Stock Jumped 9% Near a Record While Trading Above Wall Street’s Target. Here’s Where the Stock Could Go in 2026

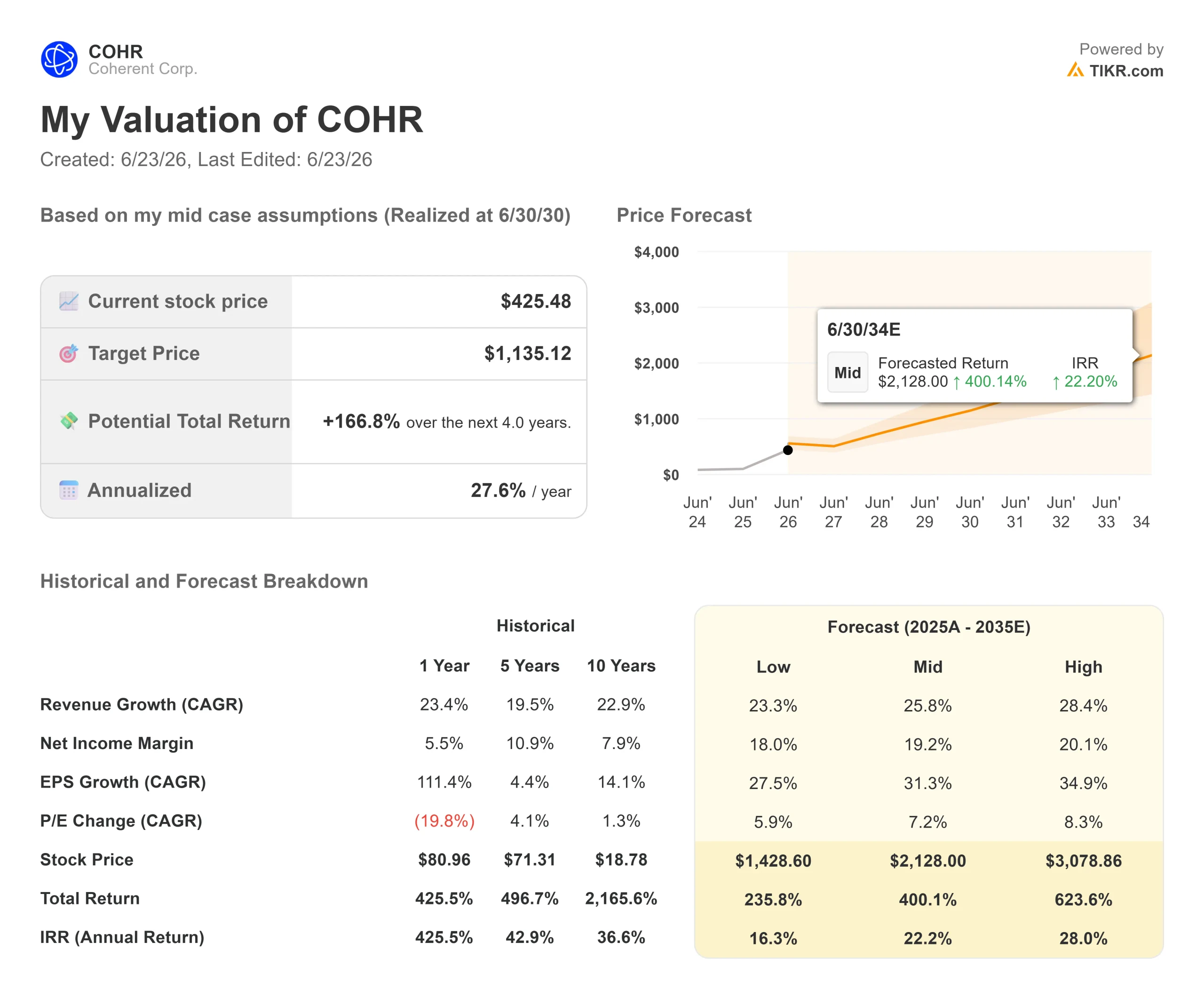

Key Stats for Coherent Stock

- Current Price: $425.48

- Target Price (Mid): ~$1,135

- Street Target: ~$385

- Potential Total Return: ~167%

- Annualized IRR: ~28% / year

- Earnings Reaction: -7.39% (May 6, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Coherent (COHR) closed June 22 up 9.22% at $425.48, within a few dollars of its all-time high, and the move exposed a standoff. The stock now trades above the average analyst target of around $385. For a name this widely covered, that is rare. It means the market is pricing in a future that Wall Street’s models have not caught up to.

The optimism has a source. Optical stocks rallied that session after Bank of America raised its 2030 AI data center addressable market estimate to roughly $1.7 trillion from about $1.4 trillion, lifting targets across the group. For Coherent, that landed on top of fresh news that gave the AI story a domestic-manufacturing spine.

The CHIPS Act Signal

On June 16, Coherent signed a letter of intent to receive up to $50 million in CHIPS Act funding, the federal program subsidizing U.S. chip production, to expand its indium phosphide plant in Sherman, Texas. Indium phosphide, the compound semiconductor at the heart of Coherent’s lasers, is the supply bottleneck for the entire optics industry. The expansion is designed to double manufacturing space and quadruple wafer capacity.

The dollar figure is small against Coherent’s spending, so this is a strategic signal more than a financial windfall. It deepens the company’s tie to both Washington and NVIDIA, since the Sherman site ramps the high-power laser production feeding their co-packaged optics partnership. CEO Jim Anderson tied it to demand: “AI is transforming our world and driving a new era of American manufacturing to build the infrastructure that will power the AI datacenters of the future.”

Coherent Revenues & Gross Margins (TIKR)

Coherent Revenues & Gross Margins (TIKR)

See historical and forward estimates for Coherent stock (It’s free!) >>>

The Quarter Backs the Move

The rally is not running on headlines alone. Coherent’s fiscal Q3 2026, reported May 6, was a record: revenue of $1.81 billion (up 21% year-over-year) and non-GAAP EPS of $1.41 (up 55%). The Datacenter & Communications segment grew more than 40% year-over-year and made up 75% of revenue, with gross margin expanding to 39.6%.

Visibility stood out more than growth. Anderson described “another step function increase in our order book,” with orders now reaching into calendar 2028. The capacity ramp is ahead of plan: management expects to double internal indium phosphide output a quarter early, then more than double it again by the end of 2027. The reason it matters for margins is blunt in Anderson’s words: “6-inch versus 3-inch is more than 4x as many devices at less than half the cost.” That one line explains both the revenue runway and the margin expansion.

The stock actually fell 7.39% the day Q3 landed, as the market first balked at guidance. Its recovery to near a record shows the reaction reset, not the thesis.

The Valuation Tension

The other side is hard to dismiss. Coherent trades around 178 times trailing earnings, and the Street’s average fair value of roughly $385 sits below the current price. Yet sentiment is firmly bullish: 13 analysts rate the stock Buy and 4 Outperform, against 4 Holds and no Sells. The premium is real, and so is the conviction behind it.

Peers frame the stretch. Coherent’s NTM EV/EBITDA of 38.04x runs above Corning at 33.71x and Fabrinet at 31.65x, well past the peer median of 21x. Its NTM P/E of 57.16x sits above Eoptolink at 32.45x. That premium is defensible only if Coherent’s growth and margins genuinely outpace the group, which the 6-inch cost edge and the NVIDIA-anchored pipeline argue they will. That is a case, not yet a proof.

Coherent NTM EV/EBITDA (TIKR)

Coherent NTM EV/EBITDA (TIKR)

See how Coherent performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $425.48

- Target Price (Mid): ~$1,135

- Potential Total Return: ~167%

- Annualized IRR: ~28% / year

Coherent Advanced Valuation Model (TIKR)

Coherent Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Coherent stock (It’s free!) >>>

Two revenue drivers carry the forecast: the transceiver ramp across 800-gig and 1.6T (the data rates moving AI traffic inside data centers), and the newer layers in co-packaged optics, optical circuit switches, and multi-rail. The margin driver is the shift to 6-inch indium phosphide, which lowers unit cost as it scales. The case assumes a revenue CAGR of around 26% and a net income margin near 19%.

The upside: if co-packaged optics and the capacity ramp convert backlog on schedule, the model’s high case points steepen.

The downside: any slip in hyperscaler spending or 6-inch yields would hit a stock priced for near-flawless execution.

Conclusion

Watch fiscal Q4, reported in August. Management guided revenue to $1.91–$2.05 billion and EPS to $1.52–$1.72, both implying acceleration in Q3. “Good” looks like revenue at the high end with gross margin pushing toward 41%, proof that the 6-inch ramp is converting to profit. “Bad” looks like a guide-down or margin stall, which a stock at 178 times earnings and above its own analyst target would struggle to absorb. August decides whether the fundamentals justify the premium or puncture it.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Coherent?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Coherent, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Coherent alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Coherent on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Carnival (CCL) Stock: Revenue Miss Overshadows Earnings Beat as Shares Slide

Target (TGT) Stock Surges After Wolfe Research Elevates Rating to Outperform

Buy, Sell, or Hold: SanDisk at $2,184 and Micron at $1,134