Starbucks Wants 10,000 More US Stores. Here’s What SBUX Stock Could Do in 2026

Key Stats for Starbucks Stock

- Current Price: $104.60

- Target Price (Mid): ~$137

- Street Target: ~$106

- Potential Total Return: ~31% (over roughly 4 years)

- Annualized IRR: ~6% / year

- Earnings Reaction: +8.45% (April 28, 2026)

- Max Drawdown (1Y): 19.06% (October 10, 2025)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Starbucks Corporation (SBUX) has spent the past year convincing investors that its turnaround is real. Now it wants them to believe something bigger: that the world’s largest coffeehouse chain, with more than 41,000 locations, is still a growth company. That is a harder sell. The stock trades near $105, recovered from an October low, yet still sits below where it traded in 2019. Bulls see a brand finally executing again, with a runway management says could add 10,000 US stores and double the international base. Bears see a mature retailer at almost 80 times earnings, fighting unionized labor and thin margins. The question the market cannot yet answer is whether the next leg of growth is real expansion or a story stapled onto a recovery that is already priced in.

That tension came into sharp focus on June 9, when CEO Brian Niccol sat down at the Evercore Consumer and Retail Conference and laid out a unit-growth case more aggressive than anything in the recent “Back to Starbucks” messaging. The headline number: Starbucks believes it can add 10,000 stores in the United States alone, on top of a global base it thinks can double overseas.

The growth story management is actually telling

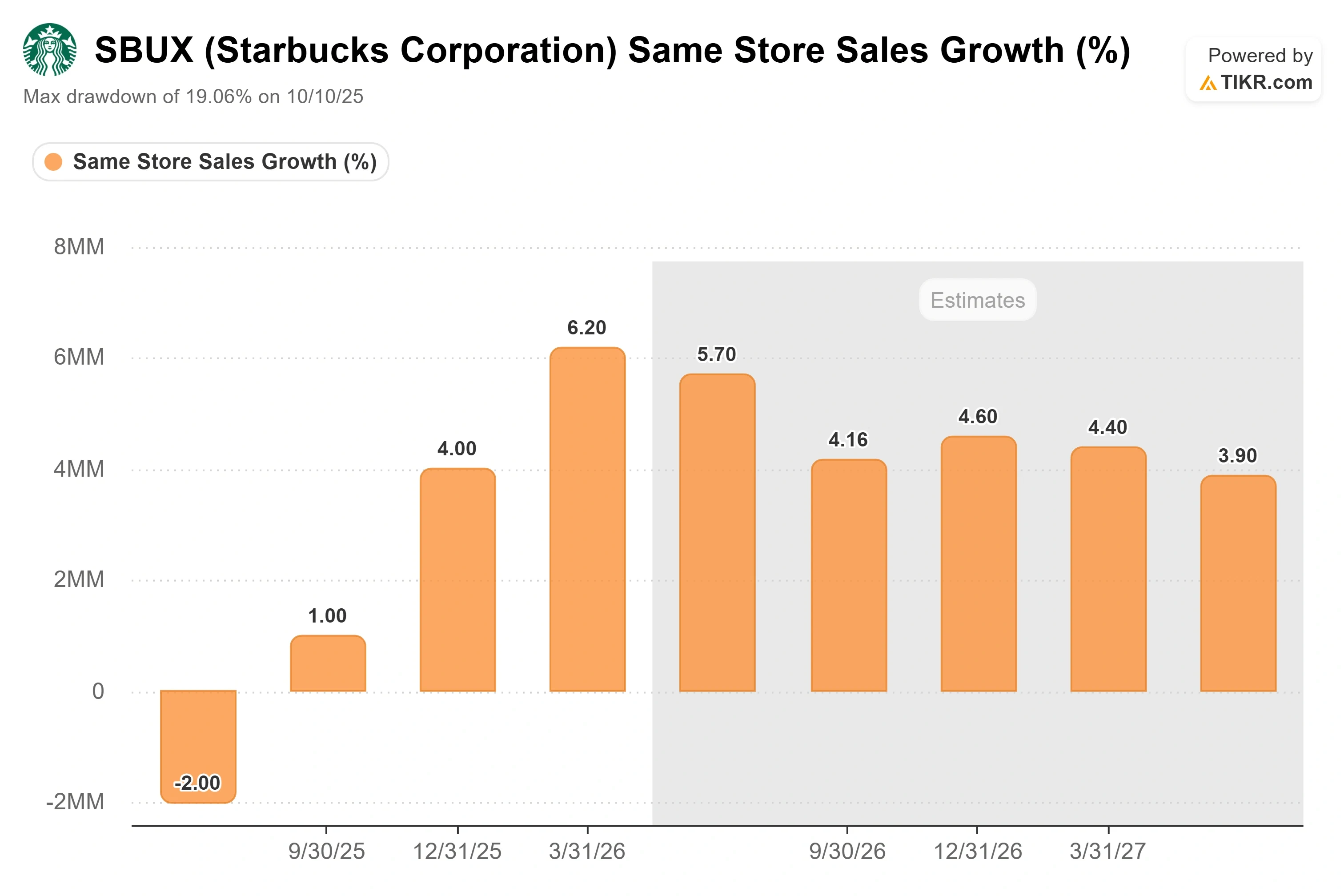

The turnaround part is no longer in dispute. In the second quarter of fiscal 2026, reported on April 28, global comparable sales grew around 6%, North America comps accelerated to around 7%, and earnings per share rose to $0.50, the first quarter of simultaneous top- and bottom-line growth in more than two years. The stock jumped 8.45% that day. Transaction growth, not price increases, drove most of the gain, which is the harder and more durable kind of comp.

What Niccol added at Evercore was a map of where growth goes from here. He pointed to a US store base concentrated on the coasts and thinning through the middle of the country. “We’re really underpenetrated in the middle of the country,” he said, citing Nashville as an example where the company has almost no corporate stores in a market that could support a dozen or more. Stack the underpenetrated geography on top of new, smaller-format stores, and the math gets large. “That’s how you get to 10,000 additional stores in the US,” Niccol told investors. He added that the roughly 22,000 stores outside the US could double over time, with the China partnership alone targeting a move from 8,000 stores toward 20,000.

The second growth lever is time of day, not geography. Around half of Starbucks’ business happens before 10 a.m., and around 65% before noon. The afternoon is largely untapped. Niccol framed the goal plainly: “I’d love the afternoon peak to be as powerful as the morning peak.” Getting there depends on two fixes management says are still in progress. The supply chain needs daily deliveries and sub-24-hour replenishment in every store, up from around 60% of stores today, so that food and refreshers stay in stock. And the stores themselves need the “uplift” remodels that put seating back in and make the coffeehouse a place people linger. Niccol said the uplifts are coming in at $150,000 or less per store and already driving a transaction uptick, a far better return than the older, costlier remodel program.

Starbucks Revenue & EBITDA (TIKR)

Starbucks Revenue & EBITDA (TIKR)

See historical and forward estimates for Starbucks stock (It’s free!) >>>

Why the market is not paying for it yet

Here is the disconnect. The growth runway is ambitious, but the stock is priced as though the recovery is the whole story. Starbucks trades at an NTM (next twelve months) price-to-earnings ratio of around 39x and a trailing P/E near 80x, both elevated because earnings are still depressed from the labor-investment cycle. That makes the stock look expensive on today’s numbers and cheap only if you believe the forward story. The Street is hedging. The mean analyst target is around $106, barely above the current price, with the high target at $137 and the low at $81. Of the analysts tracked by TIKR, the breakdown is 12 buys, 5 outperforms, 16 holds, 2 underperforms, and 2 sells. That is a consensus waiting for proof, not chasing a story.

The bear case is not just about valuation. Gross margins compressed to around 20% in the second quarter from around 23% a year earlier, squeezed by product costs and tariff-related inflation. North America’s operating margin remains roughly half its pre-investment level. And the labor relationship is openly hostile: on June 18, Starbucks filed a federal trademark lawsuit against Starbucks Workers United in Iowa, accusing the union of diluting its siren logo. The suit, which counters one the union filed in April, signals that stalled contract talks and the risk of further strikes are not going away. For a company whose entire thesis rests on consistent in-store execution, ongoing labor unrest is a direct threat to the comp recovery.

Against peers, the premium is real but not indefensible. Starbucks trades at an NTM EV/EBITDA of around 24x, well above Yum! Brands at around 17x, Chipotle at around 20x, and Restaurant Brands at around 13x, though below high-growth Dutch Bros at around 28x. The question is whether a mature 41,000-store chain deserves a multiple closer to the fast growers than the established franchisors. The answer depends entirely on whether the unit-growth and afternoon-daypart story Niccol outlined actually materializes. If it does, the multiple is justified. If growth stays mid-single-digit, it is not.

Starbucks Same Stores Sales Growth (TIKR)

Starbucks Same Stores Sales Growth (TIKR)

See how Starbucks performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $104.60

- Target Price (Mid): ~$137

- Potential Total Return: ~31%

- Annualized IRR: ~6% / year

Starbucks Advanced Valuation Model (TIKR)

Starbucks Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Starbucks stock (It’s free!) >>>

The two revenue drivers are unit growth and the afternoon daypart: new, smaller-format US stores plus international expansion supply the volume, while a second daily sales peak built on refreshers and food lifts revenue per store. The model uses revenue growth of around 5% (CAGR) in the mid-case. The margin driver is operating leverage as the Green Apron Service labor investment annualizes in the fourth quarter of fiscal 2026, and the $2 billion cost-savings program flows through, lifting net income margin toward around 10%. The primary risk is that margin recovery stalls if labor unrest disrupts execution or if input costs stay elevated.

The upside: if the afternoon daypart and store expansion deliver while margins normalize, the high case points to around $205, a return well north of the mid case.

The downside: if growth stays mid-single-digit and the multiple compresses, the low case sits near $140 on price but only around 4% annualized, meaning you wait years for little

Conclusion

The turnaround is proven. The growth story is not. The single number that will confirm or break the next phase is North America transaction growth in the fiscal third-quarter report, expected in late July 2026. Two consecutive quarters above 4% transaction growth, which is what the company posted in Q2, would signal that the recovery is durable enough to support the expansion Niccol is promising. Anything that slips back toward flat would tell investors the afternoon-daypart and 10,000-store narrative is running ahead of the business. Watch the transactions, not the headline comp. That is where the next leg of this stock gets decided.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Starbucks?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Starbucks, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Starbucks alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Starbucks on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Monday Market Wrap: Comcast Breakup, Alphabet’s Dow Debut, and Tech Stock Rally

Columnist cracks the 'unifying theory' behind Trump's seemingly manic behavior: opinion