Up 140% YTD, Three Catalysts Will Take AMD to New Highs In 2026

The post Up 140% YTD, Three Catalysts Will Take AMD to New Highs In 2026 appeared first on 24/7 Wall St..

Advanced Micro Devices (NASDAQ:AMD) has become the semiconductor story of 2026. Shares are up 152.56% year-to-date, driven by an AI infrastructure buildout that keeps expanding faster than the market can price in.

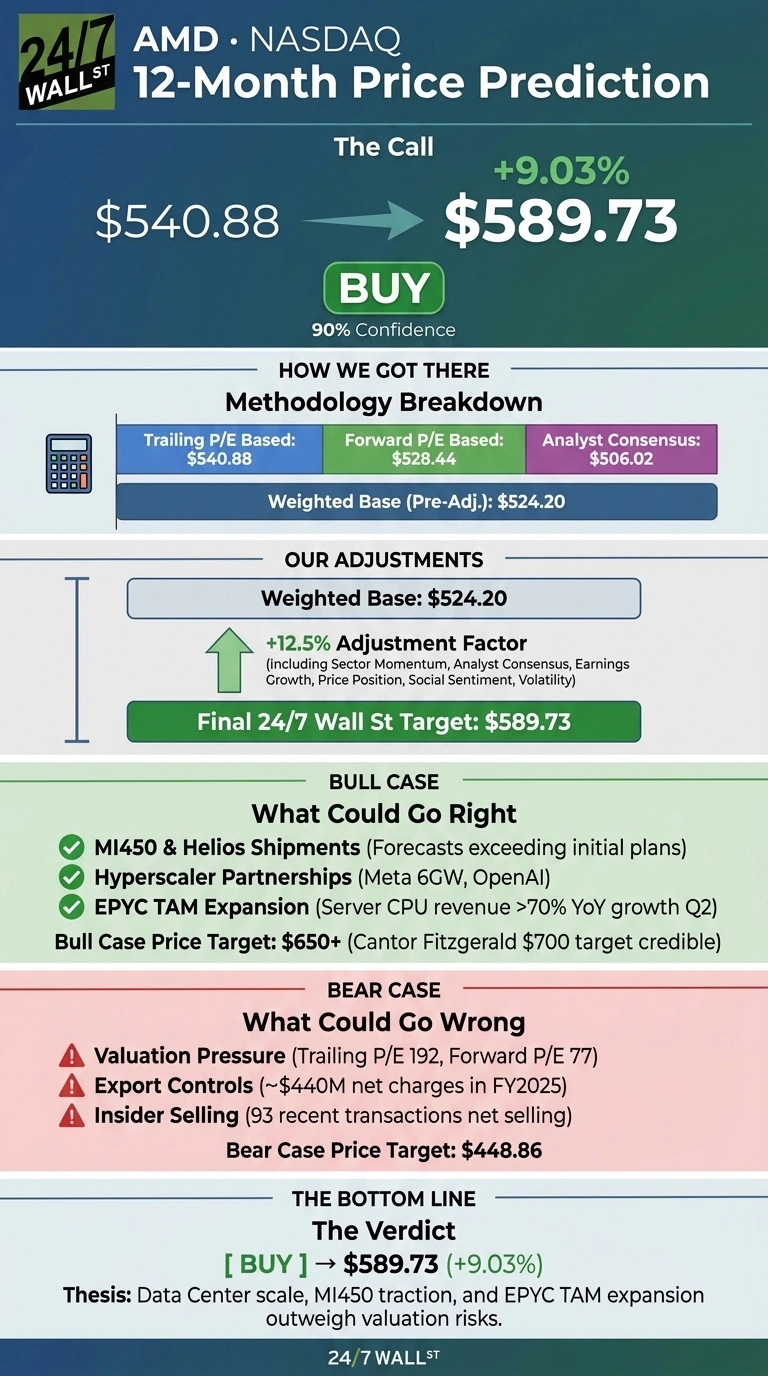

Our 24/7 Wall St. price target for AMD is $589.73, roughly 9.03% above where the stock trades today. Our model rates AMD a buy, backed by a 90% confidence score.

24/7 Wall St.

24/7 Wall St.

| Metric | Value |

|---|---|

| Current Price | $540.88 |

| 24/7 Wall St. Price Target | $589.73 |

| Upside | 9.03% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Blowout Q1 Reset the Growth Curve

Q1 2026, reported May 5, 2026, was the inflection point. AMD delivered revenue of $10.25 billion, growing 37.85% year-over-year, with non-GAAP EPS of $1.37 beating consensus by 5.88%. Data Center revenue jumped 57% to $5.78 billion, and free cash flow more than tripled to $2.57 billion.

Management guided Q2 revenue to approximately $11.2 billion, or roughly 46% YoY growth. Recent tailwinds keep piling on: a 30 MW Rackspace deployment, a 50 MW Riot Platforms agreement, and analyst upgrades from Wells Fargo ($615), UBS ($670), and Cantor Fitzgerald ($700).

The Case for $650+

Three catalysts anchor the bull thesis. First, MI450 and Helios: Lisa Su told investors “lead customer forecasts now exceeding our initial plans”, with Helios shipments ramping in H2 2026.

Second, hyperscaler wins. The 6-gigawatt Meta partnership spans several product generations, and the OpenAI relationship positions AMD, per Su, as “a core partner to the world’s largest AI infrastructure builders”.

Third, EPYC. Su now expects the server CPU TAM to grow greater than 35% annually, reaching over $120 billion by 2030, with server CPU revenue guided to grow more than 70% YoY in Q2. Cantor’s $700 target represents a credible bull case.

What Could Go Wrong

Valuation is the obvious pressure point. AMD trades at a trailing P/E of 192 and a forward P/E of 77, and shares fell 6.89% on July 1 in a broad chip pullback. Export controls on MI308 to China cost around $440 million in net inventory charges last year, and TSMC dependence remains a supply-chain single point of failure.

Insider selling has also picked up, with 93 recent transactions net selling. Bulls would counter that these charges are non-recurring, that TSMC’s 10-year Arizona packaging deal with Amkor materially de-risks capacity, and that heavy insider distribution typically follows an explosive rally.

A bear scenario lands near $448.86, roughly 17% below current levels.

The Bottom Line on AMD

The 24/7 Wall St. price target of $589.73 reflects a buy rating at 90% confidence. Data Center scale, MI450 traction, and EPYC TAM expansion together outweigh the valuation risk in my view.

Key items to watch: whether Helios shipments track on schedule in H2 and whether MI450 forecasts keep beating internal plans. Risks to monitor include tighter China export policy or softer hyperscaler capex signals into 2027.

AMD Price Prediction 2026-2030

Extending the model forward, assuming Lisa Su’s target of tens of billions of dollars in annual Data Center AI revenue in 2027 and long-term gross margins of 55% to 58%:

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $589.73 |

| 2030 | $753.37 |

These projections assume AMD continues executing on MI450, Venice EPYC, and hyperscaler ramps. Significant upside or downside could result from AI capex cycles, China export policy, or share gains against ARM-based competition.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and AMD didn’t make the cut. Grab the names FREE today.

The post Up 140% YTD, Three Catalysts Will Take AMD to New Highs In 2026 appeared first on 24/7 Wall St..

You May Also Like

Altcoin Sell Pressure Hits Multi-Year Low, Says CryptoQuant

How Cloudflare Is Positioning for the AI Era