Dell Stock Fell 7% in a Day. Is the AI Margin Fear Real or an Opening?

Key Stats for Dell Stock

- Current Price: $394.32

- Target Price (Mid): ~$530

- Street Target: ~$485

- Potential Total Return: ~35%

- Annualized IRR: ~7% / year

- Earnings Reaction: +21.93% (February 26, 2026)

- Max Drawdown: 32.64% (January 20, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Dell Technologies (DELL) just had the kind of day that makes new buyers flinch. The stock fell 7.27% on July 2, 2026, closing at $394.32, and the reason had nothing to do with a bad quarter. Dell’s business is running hot. The argument is about the one number bulls would rather not discuss: gross margin.

That is the tension pulling this stock in two directions right now. On one side, Dell is the box maker at the center of the AI buildout, with a record backlog and an order book that outruns supply. On the other hand, every dollar of that AI server revenue carries a thinner margin than the servers and storage Dell used to sell. The market cannot yet decide whether that trade-off is a temporary cost of winning or a permanent dent in the profit engine.

Dell has now given back roughly 16% from its 52-week high of $469.47, and the slide has been steady rather than sharp, the pattern of a market letting air out rather than panicking. The drop also came with a governance overhang, because insiders sold roughly $1.56 billion in shares over three months with no matching purchases.

The margin fear has a face, and it is the AI server mix

Here is the worry in plain terms. In the first quarter of fiscal 2027, Dell’s gross margin compressed to about 18% from about 21% a year earlier, and management pinned it on the shift toward lower-margin AI-optimized servers, the high-powered machines built to train and run AI models. AI server revenue that quarter reached about $16 billion, up roughly 760% year over year. That is spectacular growth attached to a thinner slice of profit per dollar, and it sat at the center of the July 2 sell-off alongside profit-taking and the insider selling noted above, even with no fresh bad news of Dell’s own that day.

The debate got a headline on June 25, 2026, when GF Securities cut Dell to Hold from Buy. Analyst Jeff Pu argued that after a rally of roughly 200% since February, the good news was already in the price. At the time of that call, the stock traded near 34 times trailing earnings, well above its longer-run median, closer to 13 times. For context, TIKR data now puts Dell at 31.52 times trailing earnings and 21.28 times forward earnings after the recent pullback. The stock gapped lower on heavy volume that day, and the July 2 drop was the same fear resurfacing, sharpened by a broad slide in memory and hardware names as rising DRAM and NAND chip costs threatened input margins across the group.

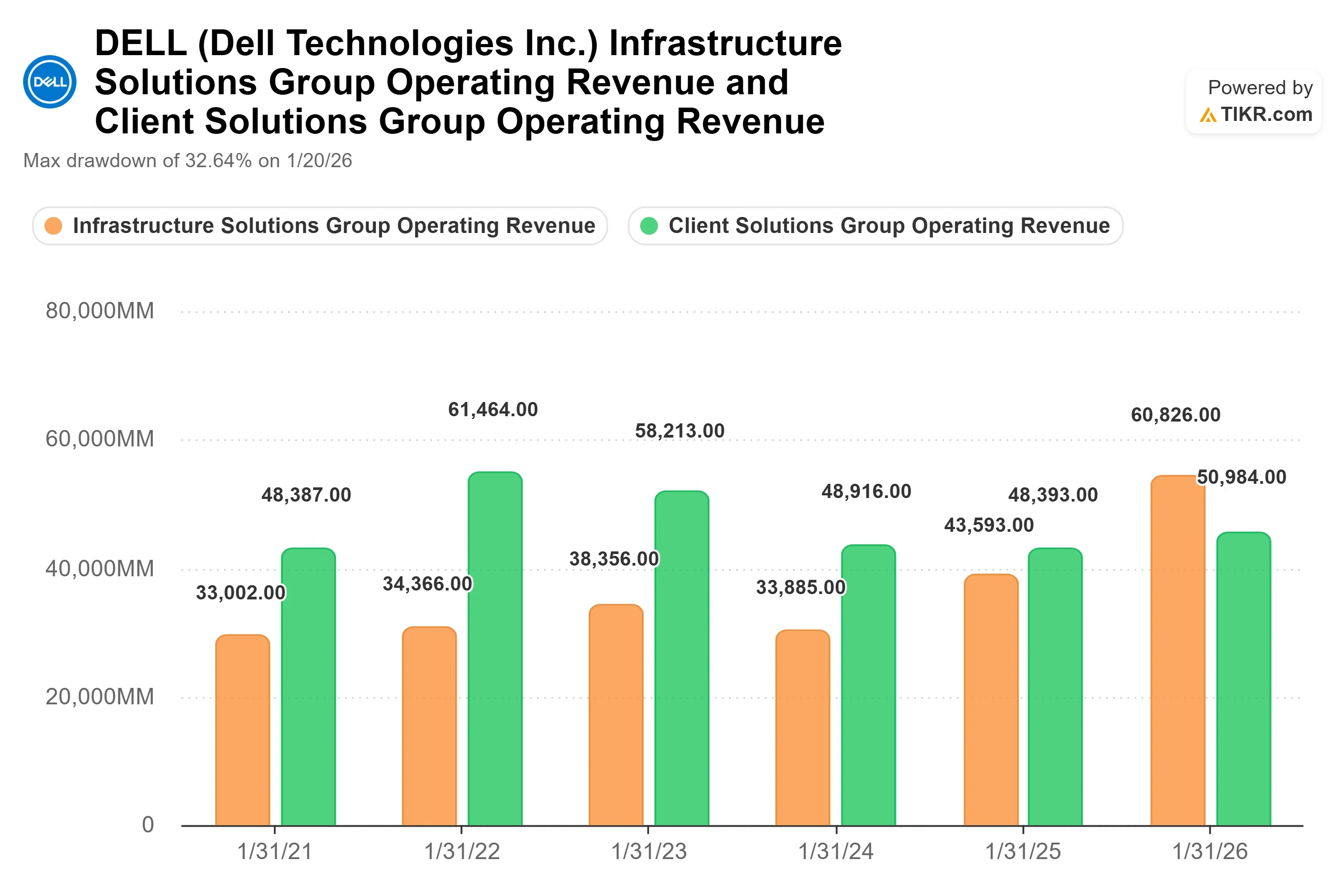

Dell ISG & CSG Operating Revenue (TIKR)

Dell ISG & CSG Operating Revenue (TIKR)

See historical and forward estimates for Dell stock (It’s free!) >>>

What management actually said about margins

This is where the picture gets more interesting than the headline. At the Bank of America Global Technology Conference on June 2, 2026, Arthur Lewis, who heads Dell’s Infrastructure Solutions Group (ISG), the segment that houses servers, storage, and networking, addressed the margin question directly. His answer was not a deflection. It was a specific claim that the fear is misreading the business.

Lewis said Dell moved its entire server business into a new cost structure on December 9, once it saw memory inflation was not a passing spike. On margins, he said, “we’re actually below where we were in COVID,” framing current server profitability as inside historical ranges rather than deteriorating. That matters because it reframes the compression as a mix effect layered on stable underlying margins, not a collapse in pricing power.

The second half of his argument is the part the market keeps ignoring: storage. Lewis pointed to Dell-owned intellectual property storage as “one of the bigger lever in the overall ISG profitability framework,” noting Dell IP storage has grown ahead of the market on a demand basis for five straight quarters. Dell IP storage carries richer margins than the partner-branded storage Dell also resells. So even as AI servers dilute the blended margin, a growing, higher-margin storage business is quietly pushing the other way.

A storage deal landed the same day the stock fell

The timing here is almost too neat. On July 2, 2026, in the same session, Dell dropped 7%, the company disclosed a deal to modernize NTT DOCOMO’s core infrastructure onto Dell PowerStore and PowerMax storage, a migration projected to cut the carrier’s seven-year infrastructure costs by more than 50%. It is a live proof point for the exact storage-margin lever Lewis described a month earlier. One data point is not a thesis, but it is the kind of Dell IP storage win that widens margins rather than thinning them.

What the valuation actually looks like next to peers

Dell trades at around 14.5 times next-twelve-month EV/EBITDA (enterprise value against forward earnings before interest, taxes, depreciation, and amortization). That sits above the technology hardware peer median of roughly 9.3 times, so Dell carries a clear premium to the broad group. Against storage specialists, it looks different: Western Digital trades near 22.9 times and Seagate near 26 times on the same measure, so Dell is far from the most expensive name in its neighborhood.

Whether the premium is earned comes down to growth, and this is where the numbers do the arguing. Dell’s forward two-year revenue CAGR sits near 30%, a pace most hardware peers cannot approach, and its forward two-year EPS CAGR runs above 44%. A scale leader growing revenue at 30% while slower rivals grow single digits can defend a premium. The risk is that the premium quietly assumes the AI server surge holds for years, and hardware cycles have a long history of pulling demand forward and then handing it back. That risk is why some Wall Street coverage now frames the debate as valuation, not execution.

The bear case is not that Dell is a bad business. It is that the market has priced years of flawless AI execution into a stock where the profit per dollar of that AI revenue is structurally lower than the business it replaced. The bull case is that the storage margin engine, the supply-gated backlog, and stabilizing server margins mean the compression fear is looking at the mix and missing the money.

Dell Gross Margins & Operating Margins (TIKR)

Dell Gross Margins & Operating Margins (TIKR)

See how Dell performs against its peers in TIKR (It’s free!) >>>

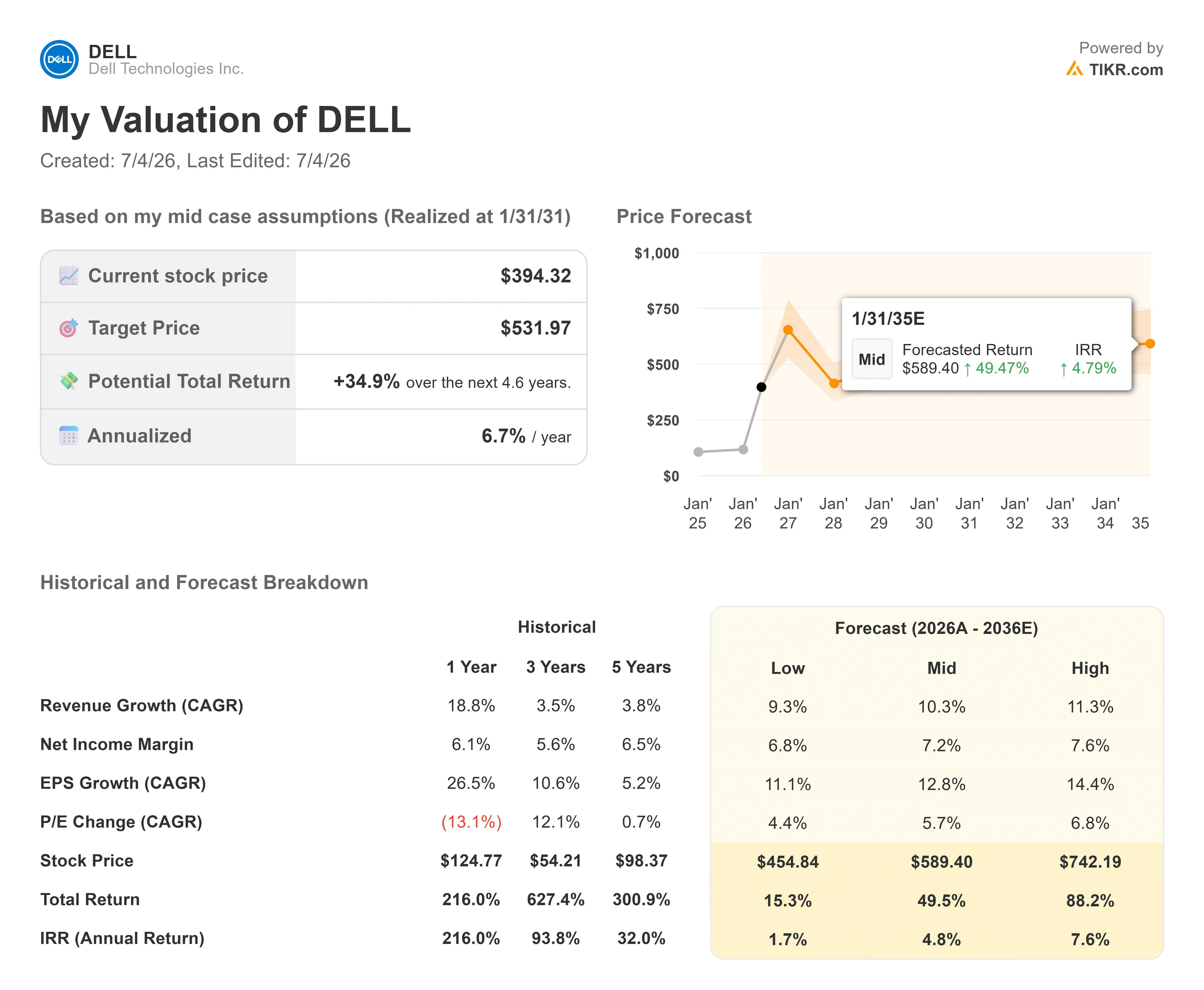

TIKR Advanced Model Analysis

- Current Price: $394.32

- Target Price (Mid): ~$530

- Potential Total Return: ~35%

- Annualized IRR: ~7% / year

Dell Advanced Valuation Model (TIKR)

Dell Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Dell stock (It’s free!) >>>

Using the TIKR Valuation Model mid case, realized at January 31, 2031, Dell’s fair value lands near $530, about 35% above the current $394.32, for an annualized IRR of roughly 7% per year. That is a positive but not heroic return, which fits a stock that has already run hard.

Two revenue drivers carry the model. The first is AI-optimized server demand, where Dell guides to around $60 billion in AI server revenue this fiscal year against a supply-gated backlog. The second is Dell IP storage, growing ahead of the market for five straight quarters and mixing toward higher-value, Dell-owned products. The margin driver is that same storage shift, which offsets AI server dilution and holds blended profit margins steadier than the headline compression suggests.

The primary risk is demand durability: if the AI server cycle pulls forward and then cools, both the revenue growth and the premium multiple compress at once. The upside case is that supply-gated AI demand plus a widening storage margin lever pushes fair value toward the model’s high scenario, near $740. The downside case is that margin compression proves structural rather than mix-driven, and the model’s low scenario near $455 becomes the ceiling instead of the floor.

Conclusion

The whole argument resolves at one event: Q2 fiscal 2027 earnings, expected in late August 2026. Watch ISG gross margin. If it holds near current levels or ticks up while AI server revenue lands around management’s roughly $15.5 billion quarterly pace, Lewis is right that the compression is a mix effect, not a leak, and the July sell-off looks like a gift. If the margin slips further as the AI mix climbs, the bears who called the top get their proof. One number in late August decides which side the data is on.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Dell?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Dell, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Dell alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Dell on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Lawyers remain in disbelief over ‘fascist Hellscape’ July 4 display in DC

LIST: Bayanihan initiatives amid soaring oil prices

Trump's billion-dollar crypto gain came with almost $4B investor losses