IREN Stock Jumped 13% in a Day on an Anthropic Australia Report. Here’s Where the Stock Could Go in 2026

Key Stats for IREN Limited Stock

- Current Price: $43.91

- Target Price (Mid): ~$325

- Street Target (Mean): ~$81

- Potential Total Return: ~639%

- Annualized IRR (Mid): ~65% / year

- Earnings Reaction: +7.65% (May 7, 2026)

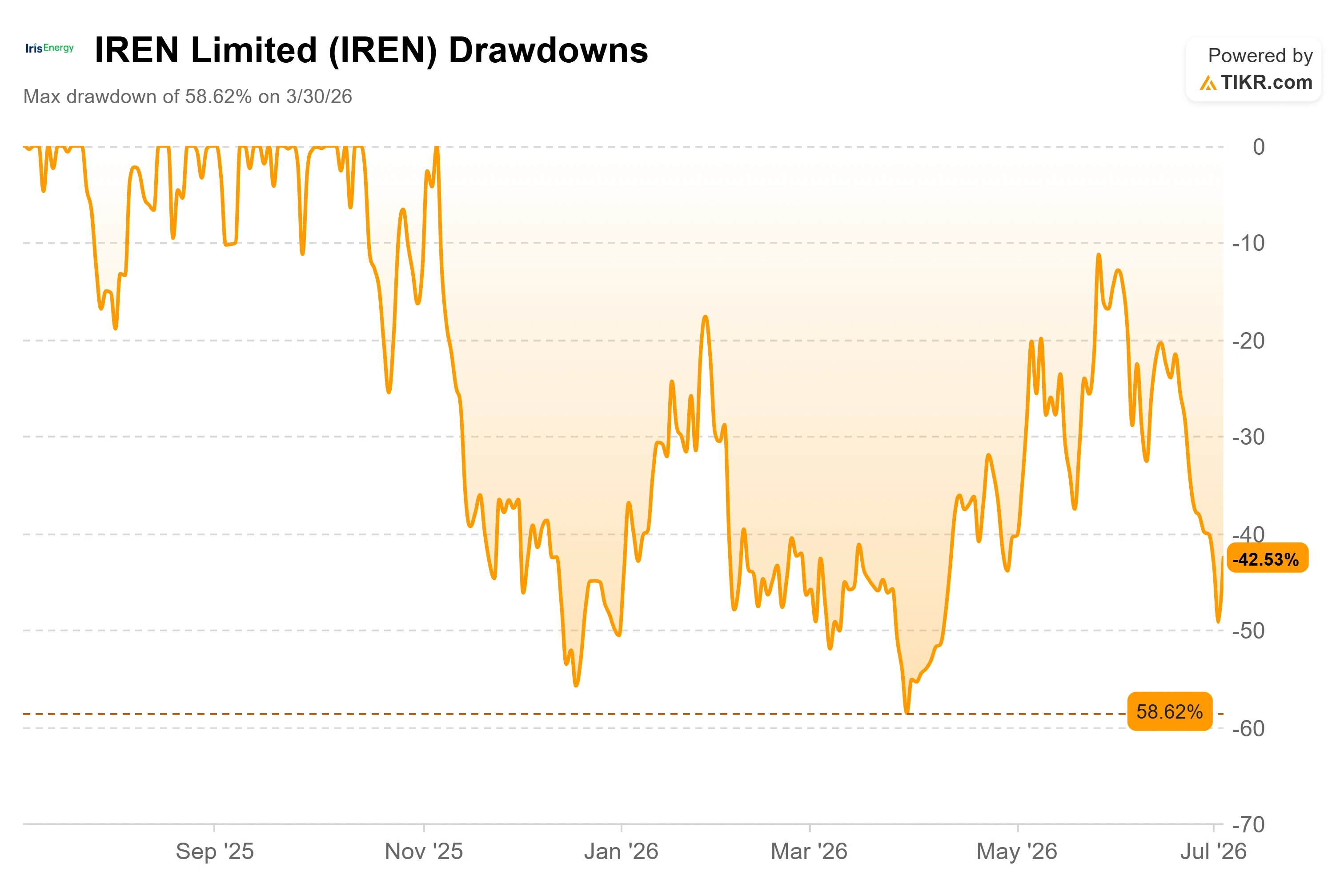

- Max Drawdown: 58.62% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

IREN Limited (IREN) is a stock the market cannot decide whether to love or fear, and on Monday both instincts collided. Shares closed at $43.91 on July 6, up 13.11% in a single session. That pop snapped a nine-day losing streak, and it came after a slide that took the stock from near $61 in mid-June to $38.82 by July 2. Even with Monday’s jump, IREN finished the trailing week lower. For a company this size, that is a violent round trip in three weeks.

The move was not random. It followed a weekend report that Anthropic, the AI lab behind the Claude models, is running a private tender for at least 1.4 gigawatts of Australian data center capacity, a project valued at roughly $12 billion to $15 billion. IREN was named on the shortlist of bidders. The market read that as validation of the one part of IREN’s story that has always been more promise than proof: its Australian ambitions.

Here is the tension. IREN is not a landlord waiting for tenants. It builds and operates its own AI cloud on the power it already controls. That model is why bulls see a generational infrastructure winner. But the Anthropic headline is a reported request for proposals, not a signed contract, and the stock still trades 42.53% below its 52-week high of $76.87. The question the market cannot yet answer is simple: is this the moment IREN’s secured power finally converts into the kind of revenue that justifies the valuation, or is a rumor doing the work the fundamentals have not?

What the Anthropic tender actually says

According to The Australian Financial Review’s Street Talk column, which reviewed the confidential documents, Anthropic circulated a request for proposals to a small group of Australian operators including CDC Data Centres, AirTrunk, NextDC, IREN, and Stack. Anthropic wants at least 1 gigawatt of capacity operational by the end of 2027 and may split the award across four or five providers rather than choosing a single winner. The report noted Anthropic is at least six weeks from a final decision.

That last detail matters. This is optionality, not backlog. Infratil-owned CDC Data Centres is widely expected to secure the largest share if the deal is divided. IREN’s claim to a seat at the table rests on its 800-megawatt Bundey campus in South Australia, where a transmission connection agreement is already secured. Being shortlisted alongside established real estate operators validates IREN’s pivot, but it does not guarantee a signed lease.

The reason the shortlist is credible ties directly to what management said on its most recent earnings call. On IREN’s Q3 FY2026 call, Co-Founder and Co-CEO Daniel Roberts framed Asia Pacific as the next frontier: “Australia looks like a fantastic frontier for us, and we’ll look to accelerate that in parallel with North America and Europe.” He was explicit that IREN has been progressing large-scale Australian grid access for some time, and described the region’s infrastructure requirement as enormous and “largely unmet.” A tender from a frontier AI lab is exactly the demand signal that the thesis predicted.

IREN Limited Drawdowns (TIKR)

IREN Limited Drawdowns (TIKR)

See historical and forward estimates for IREN Limited stock (It’s free!) >>>

Why the market keeps whipsawing this stock

IREN sits at the intersection of two of the most volatile trades in the market: crypto and AI infrastructure. When sentiment in either turns, the stock moves hard. That is why it fell almost 20% over the week before Monday’s rebound, then snapped back 13% on one headline.

Underneath the volatility, the operating story is changing fast. IREN is winding down Bitcoin mining and standing up AI cloud, and the transition creates messy quarters. In fiscal Q3, reported March 31, 2026, revenue was $144.80 million, missing consensus by 33.89%, and the company posted a GAAP net loss of $247.8 million. Yet the stock rose 7.65% the day it reported. The market looked through the loss because $140.4 million of it was a non-cash impairment on retired mining rigs, and because AI cloud revenue nearly doubled sequentially to $33.6 million. Adjusted EBITDA still came in at $59.5 million.

That gap between headline losses and underlying momentum is the whole point. IREN trades on contracts and capacity, not current earnings. The free cash flow picture is deeply negative while the build-out runs, and that is the bear case in one number. IREN needs capital markets to stay open. The bull case answers that the funding template already works: management financed roughly 95% of its Microsoft GPU capital expenditure through prepayments and GPU financing at an average rate of about 3%, a structure Roberts called a “great template” for future deals.

The signed backlog behind the speculation

Strip out the Anthropic rumor, and IREN still has real contracted revenue. The company reported $3.1 billion of annual recurring revenue (ARR), meaning revenue it expects to collect on an annualized basis under existing contracts, and reaffirmed a target of $3.7 billion exiting calendar 2026. That backlog includes the $9.7 billion Microsoft deal and a new $3.4 billion five-year AI cloud contract with NVIDIA announced during the quarter. Management also secured 5 gigawatts of power globally and framed the demand environment bluntly: “We are not chasing demand. We are racing to build supply fast enough to meet it.”

Roberts drove the scarcity point home with a line that captures the entire thesis: “There are no idle GPUs.” He argued the constraint is not finding customers but delivering compute, because “a customer contract doesn’t deliver revenue. Having compute online delivers revenue.” That is why the metric IREN tracks above all others is what it calls time to compute, the speed from secured power to live, revenue-generating capacity.

On valuation, IREN screens expensive on trailing numbers and reasonable on forward ones, which is normal for a company scaling this fast. It trades at roughly 8.50x NTM enterprise value to revenue. Microsoft trades near 7.93x on the same measure, so IREN carries a modest premium to a hyperscaler with vastly more scale and actual profits. Against the neocloud peer Nebius Group (NBIS) at about 10.37x, IREN looks cheaper. The premium over Microsoft is hard to justify on fundamentals today. It only makes sense if you believe IREN’s forward revenue CAGR, which TIKR pegs at around 145% over the next two years, is real. That is the crux of the debate, and a signed Anthropic contract would move it decisively toward the bulls.

IREN Limited Bitcoin Mining & AI Cloud Service Operating Revenue (TIKR)

IREN Limited Bitcoin Mining & AI Cloud Service Operating Revenue (TIKR)

See how IREN Limited performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $43.91

- Target Price (Mid): ~$325

- Potential Total Return: ~639%

- Annualized IRR: ~65% / year

IREN Limited Advanced Valuation Model (TIKR)

IREN Limited Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for IREN Limited stock (It’s free!) >>>

That target is aggressive, and it rests on aggressive inputs. The two revenue CAGR drivers are the ramp of contracted AI cloud capacity as Microsoft’s Horizon build, and the NVIDIA deal comes online, and the conversion of IREN’s uncontracted power into new leases, where an Anthropic award would be the single largest catalyst. The margin driver is the shift from thin Bitcoin economics to high-margin AI cloud, where the model assumes net income margin expanding toward roughly 33% in the mid case. The primary risk is financing: this build-out depends on capital markets staying open while free cash flow runs sharply negative.

The upside is straightforward. If IREN converts its 5 gigawatts of secured power on schedule and lands even part of the Anthropic tender, the mid-case target looks conservative. The downside is equally clear. A slipped construction date, a stalled ARR figure, or a capital raise on worse terms than the Microsoft template would tell you the bears read the cash flow statement correctly.

Conclusion

The Anthropic tender is a story about optionality, so watch for the one event that turns optionality into backlog: a formal award. The AFR report put Anthropic at least six weeks from a decision, which lines up with an announcement window in mid-to-late August, right around IREN’s next earnings report scheduled for August 27.

Here is what good versus bad looks like. Good is a confirmed Anthropic contract, or a signed lease of similar scale, alongside ARR still climbing toward the $3.7 billion year-end target. That would prove secured power is converting to revenue on schedule. Bad is IREN missing the Anthropic shortlist cut, ARR stalling below target, or a financing raise on terms worse than the 3% Microsoft template. On a stock that just swung 20% in a week on sentiment alone, the difference between those two outcomes is the difference between $325 and a much longer wait.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in IREN Limited?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up IREN Limited, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track IREN Limited alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze IREN Limited on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Trump banned this word from the White House to appease the NRA: ex-Trump official

Kenya to monitor $19 billion in crypto transactions with new blockchain platform! What are the details?

Stable Token Jumps 28% as Market Cap Approaches $800M Milestone