Stock Rally Pauses As Attention Turns To Warsh's First FOMC

Stock Rally Pauses As Attention Turns To Warsh's First FOMC

US futures are flat, pausing after a three-day rally with investors shifting their focus to this week's FOMC meeting, Kevin Warsh's first, which begins today. As of 8:00am ET, S&P futures are up 0.1% after surging 2% on Monday; and Nasdaq futures gain 0.3%, as SpaceX continued to surge, rising 11% overnight and on track for a more than 50% jump since going public, and briefly surpassing Microsoft's market value in afterhours trading. Pre-market, most of the Mag 7 names are lower; TSLA (-1.7%) and NVDA (-0.6%) are among the laggards.The dollar slipped and Treasuries rose with bond yields 1-3bp lower and the 10Y trading 4.44%. West Texas Intermediate crude fell 3% to $78 a barrel as Goldma and Morgan Stanley cut their oil price forecasts. Base metals are also lower, while gold and silver both rise 0.7% this morning. Overnight, the main macro headline was BoJ (policy rate to 1% with the tapering plan unchanged; a bit hawkish tone in the statement; 15yr JGB added 8.5bp) and China data releases (Retail Sales and FAI both missed; HSI -1.4%). US economic data calendar includes weekly ADP employment change (8:15am), May import/export price indexes, June NY Fed services business activity and May housing starts/building permits (8:30am)

In premarket trading, SpaceX rises 7.3%, putting the stock on track to extend a rally following its blockbuster debut last week. Mag 7 stocks are mixed (Amazon +0.5%, Alphabet -0.1%, Nvidia -0.1%, Apple -0.2%, Meta -0.2%, Microsoft -0.7%, Tesla -0.8%)

- Domo (DOMO) said its board’s review determined a strategic transaction is the best way to maximize shareholder value. Shares are down 13%.

- Edgewise Therapeutics (EWTX) falls 23% after the drug developer gave results from a mid-stage trial of its experimental therapy for a heart disorder.

- Edwards Lifesciences (EW) is up 3.1% after the US government published a coverage proposal for transcatheter aortic-valve replacement, with analysts citing updates that lean positive for the space.

- Huntsman (HUN) falls 7% after it agreed to merge with chemical peer Olin in an all-stock merger of equals. Olin shares are roughly flat in premarket.

- Robinhood Markets (HOOD) gains 2% after it said it is reducing its full-time employee workforce by 10%, and also closing a small number of open roles.

In other corporate news, SpaceX has formally agreed to take over Cursor in a deal that values the AI coding startup at $60 billion, cementing a key part of Elon Musk’s efforts to catch up with rivals on coding tools. In other AI news, chipmaking giant Nvidia sold $25 billion of high-grade bonds, joining a wave of jumbo debt offerings from tech heavyweights as investors clamor to get exposure to the AI boom. Anthropic is said to have held talks with the Trump administration in a bid to lift curbs which led to the company disabling global access to its two most advanced AI models.

With the Iran war on the backburner for now, the focus on Wall Street is now turning to the first Federal Reserve meeting under Kevin Warsh. While the central bank is expected to hold interest rates steady on Wednesday, the spotlight will be on how Warsh navigates the post-meeting press conference and the outlook for inflation. Oil’s drop to the lowest since early March has erased the bulk of the gains seen during the Mideast conflict, easing inflationary pressures just as policymakers assess interest rates.

“All eyes will remain on the Fed for now and how Kevin Warsh will handle the competing pressures from rising inflation and the prospect of lower energy inflation once the Strait of Hormuz reopens,” said Joachim Klement at Panmure Liberum.

The announcement by President Donald Trump of a peace deal with Iran has opened the floodgates for investors to start to deploy the roughly $8 trillion to $9 trillion sitting in money market funds, according to Rick Rieder, BlackRock Inc.’s global fixed income chief investment officer. SpaceX’s initial public offering had already forced investors to make room in portfolios, he added.

As reported earlier, SpaceX shares surged in premarket trading, putting the firm on track to overtake Amazon.com as the fifth largest publicly traded company in the world just days after its blockbuster debut. Shares jumped as much as 19% in early trading before paring those gains to about 8% as of 7:30 a.m. in New York. The premarket gain builds on a more than 40% jump across SpaceX’s first two sessions after its record initial public offering. If it holds through the trading day, the move would lift the market value of Elon Musk’s rocket and AI company to more than $2.7 trillion, above Amazon and up nearly $1 trillion from its IPO.Today SPCX options start trading which will likely add a gamma squeeze to the overall upside pressure. Separately, SpaceX formally agreed to take over Cursor in a deal that values the AI coding startup at $60 billion, cementing a key part of Elon Musk’s efforts to catch up with rivals on coding tools.

As Bloomberg notes, when it comes to SpaceX, the message is clear - buyers care very little about any fundamental or valuation argument. It was already within striking distance of Amazon’s nearly $2.7 trillion valuation at Monday’s close, and is up a further 11% in premarket trading. Options contracts on the stock begin trading Tuesday.

Investors have trimmed allocations to global equities, according to the monthly fund manager survey by BofA strategists. A net 38% of fund managers are overweight, compared to 50% in May, and participants see the biggest tail risks as second inflation wave (34%), AI bubble (28%), disorderly rise in bond yields (19%) and geopolitical conflict (12%).

Meanwhile more are starting to pay attention to the off-balance sheet and circular nature of AI fund flows, discussed extensively here. As Bloomberg notes, after SpaceX, Anthropic and OpenAI are viewed as the most likely contenders for the next blockbuster AI IPOs — and that brings a sharpening focus on the hyperscalers that have spent the past several years becoming both their financiers and their data-center landlords. Alphabet and Amazon have Anthropic exposure through partnerships and investments, while Microsoft has a 27% stake in OpenAI.

The Bank of Japan and Reserve Bank of Australia kicked off a slate of decisions for the week. The BOJ raised its benchmark rate by a quarter percentage point to 1%, the highest level since 1995 and signaled that further policy normalization lies ahead. The yen pared gains against the dollar while local bonds fell. The RBA kept its key interest rate unchanged for the first time this year in response to signs that its trio of hikes are beginning to weigh on the nation’s economy. The Bank of England and Swiss National Bank are also widely anticipated to stand pat this week. Their decisions come after the European Central Bank last week raised rates for the first time in almost three years, with President Christine Lagarde warning inflation triggered by the Iran war is widening beyond just energy.

Meanwhile, with US and Iran preparing to sign an interim peace deal in Switzerland oil is headed for longest run of declines this year on expectations a reopening of the Strait of Hormuz will revive supply. Both Morgan Stanley and Goldman Sachs cut price outlooks for the coming quarters, with the latter now assuming Persian Gulf exports will reach pre-war levels by the end of July, a month earlier than previously forecast. Additionally, Qatar is planning to rapidly boost liquefied natural gas production once the Strait of Hormuz reopens, aiming to restore most of its export capacity within two months.

European stocks are up and the Stoxx 50 is on track for its longest winning streak of the year. The Stoxx 600 rises 0.5%; industrial and banking stocks are outperforming while automotive and retail stocks are among the biggest laggards. Here are the biggest movers Tuesday:

- Allegro.eu gains as much as 5.3%, the most since May, after Permira ended its decade-long investment in the e-commerce company, with the buyout firm offloading around 131 million shares, with a total transaction value of around $1.2 billion

- Puma shares gain as much as 5.4%, the most since June 4, after HSBC upgraded the German sportswear maker to buy from hold, citing Anta Sports’ stake as a “catalyst for unlocking significant growth opportunities

- Kinepolis shares rise as much as 7.1%, trading at their highest level in almost 10 months, after the movie theater operator had its price target raised to a new Street-high at Berenberg

- Redcare shares gain as much as 11%, adding to Monday’s 17% advance, after the German online pharmacy upgraded its outlook for the year, saying preliminary second-quarter numbers came in stronger than expected

- GEA Group rises as much as 4.6% as Deutsche Bank upgrades to buy on what is now seen as a “more compelling mismatch between the group’s resilient fundamentals and the current valuation”

- PolyPeptide gains as much as 6.4%, the most in more than two months, after Berenberg lifted its price target on the stock, citing confidence in the Swiss contract development and manufacturing organization’s full-year guidance

- Tatton Asset Management shares rise as much as 13%, the most since November 2022, to erase this year’s losses after the firm posted full-year earnings described as “impressive” by RBC Capital Markets

- DFDS falls as much as 7.3%, paring much of a rally over the last two months, as SEB Bank analysts cut their recommendation on the stock to sell, saying the transport and logistics company face “elevated” risks in the Mediterranean

- Rathbones shares fall as much as 19%, the most ever, as the investment management group pauses bringing on new clients requiring enhanced due diligence for as much as a year following talks with the Financial Conduct Authority

- Frasers Group shares drop as much as 7%, edging further off the 2024 high reached on Friday, after RBC Capital Markets downgraded the retailer, saying there’s little upside to its price target following recent gains

- Huber+Suhner declines as much as 5.6% following a downgrade to hold at Berenberg, which says that while there remains a strong investment case for the maker of telecommunications products, upside is limited

Asian stocks advanced for a third straight session after Japan raised interest rates, with investors awaiting further details on the US-Iran deal to reopen the Strait of Hormuz. The MSCI Asia Pacific Index advanced 0.5%, lifted by chipmakers and defense contractors. South Korea’s Kospi outperformed, while Japan’s Nikkei 225 closed at a record high after the Bank of Japan raised the benchmark interest rate. Australian stocks erased earlier losses to close little changed after the Reserve Bank kept rates unchanged. Elsewhere, stocks slumped in Hong Kong as data showed Chinese consumer spending fell for the first time since the pandemic. Indonesian markets were closed for a holiday, while stocks mostly rose in the rest of Southeast Asia.

In FX, the dollar inches lower, sending the euro back above $1.16. The yen reversed earlier gains against the dollar and traded near 160.30, with JGB yields rising across the curve after the BOJ hiked rates to 1% overnight.The Aussie weakened 0.3%, while the country’s 3-year yield erased an earlier advance.

In rates, treasuries advanced, supported by gains across European bonds during London morning as oil prices extend declines. With US and Iran preparing to sign an interim peace deal in Switzerland oil is headed for longest run of declines this year on expectations a reopening of the Strait of Hormuz will revive supply. Treasury yields are 2bp-4bp richer across a flatter curve with 2s10s spread 1.2bp tighter on the day. 10-year is about 3.5bp lower near 4.44%, keeping pace with bunds and gilts in the sector. Treasury auctions resume with $13 billion 20-year bond reopening; WI 20-year yield near 4.942% is ~18bp richer than last month’s new-issue auction result. IG dollar issuance slate empty so far; Monday’s eight sales totaling nearly $36 billion, including Nvidia’s $25 billion offering, left gross new-issue supply 31% ahead of last year’s pace and roughly in line with 2020’s record tempo. Focal points of US session focus include a 20-year bond auction at 1pm New York time. The BOJ hiked rates earlier, the RBA held.

In commodities, WTI crude oil futures are down more than 3% at lowest level since early March and on the worst daily losing streak of the year on the US-Iran interim deal, despite disagreement on how long restoring activity in the Strait of Hormuz will take. Brent slides toward $81/barrel and is at the lowest level since March. Gold prices are higher and comfortably above $4,300/oz.

US economic data calendar includes weekly ADP employment change (8:15am), May import/export price indexes, June NY Fed services business activity and May housing starts/building permits (8:30am)

Market Snapshot

Top Overnight News

- The US and Iran are preparing to formally sign their interim peace deal in Switzerland on Friday while the text of the MOU is yet to be released. Donald Trump said the deal can survive even if Israel attacks Lebanon. Iran claimed the US has started lifting its naval blockade, semi-official ISNA reported. BBG

- Shipowners will not resume transit through the Strait of Hormuz for weeks until they are confident that the US-Iran deal is “material”, the head of the world’s biggest tanker operator has warned. FT

- A price war is unfolding in China’s crowded artificial intelligence sector as companies cut rates or dangle promotions at a pivotal moment when falling costs and converging model capabilities are ratcheting up the competitive pressure, according to analysts. SCMP

- China's consumer spending and investment have slumped to levels unseen since the pandemic, with retail sales declining 0.6% last month from a year ago. Industrial production climbed 4.5%, driven by a boom in exports and tech-related industries, but the economy is at risk of a deeper slowdown due to weak domestic demand. RTRS

- Qatar aims to restore most of its LNG export capacity within two months of the strait’s reopening, people familiar said. BBG

- The Bank of Japan raised interest rates to a 31-year high on Tuesday in a landmark step in its policy normalization, signaling readiness to tighten further as it focuses on taming price pressures from the Iran-war-induced energy shock. The hike was the first since December and aligns the BOJ with other central banks shifting towards tighter policy to combat inflation, including the ECB. RTRS

- Australia's central bank held its cash rate steady at 4.35% on Tuesday, saying the economy was slowing in the face of tighter financial conditions but warned it might yet hike again if needed to control inflation. RTRS

- Oil companies large and small are showing new interest in committing to drill in Venezuela, after nearly six months of reluctance following the U.S. removal of Nicolás Maduro and the Trump administration’s subsequent call for them to invest. Politico

- Talks between Anthropic and Trump administration officials continued Monday without a deal to resolve the security concerns that pushed the White House to restrict access to the artificial-intelligence company’s latest model, increasing urgency on both sides to find a resolution. WSJ

Middle East News

- US President Trump posted on Truth Social "Iran has agreed to never have a Nuclear Weapon! Also, the story that the U.S. is paying Iran 300 million [sic] Dollars is Fake News, put out by the Dumocrats!!!"

- US President Trump's administration considers USD 300bln fund for Iran if deal is upheld, and incentives would be tied to Tehran's performance, including over opening up the Strait of Hormuz and nuclear talks, according to FT.

- US President Trump's close aide Bruesewitz clarified that the USD 300bln Iran reconstruction plan will only be established after Iran completely dismantles its nuclear program, ceases support for terrorist organisations and conducts significant internal reforms.

- US Vice President J.D. Vance said the memorandum of understanding between the US and Iran is a brief, one-and-a-half-page document serving as a broad framework rather than a detailed agreement, and is a very general document that requires technical talks. Vance also stated that Trump may release the US-Iran agreement before Friday and affirmed the agreement is expected to be signed on Friday.

- CIA Director Ratcliffe told US President Trump and senior administration officials that information gathered by US intelligence agencies raises serious doubts about Iran's willingness to make the concessions the US seeks in a final nuclear deal, according to Axios. Sources also stated that Trump and his team discussed intelligence gathered by US intelligence agencies, which showed the way Iranian officials were discussing the deal among themselves was inconsistent with what they were telling mediators and the US. Furthermore, Ratcliffe was not the only sceptic on Trump's senior team, as Secretary of State Rubio and Defence Secretary Hegseth expressed concerns and raised questions about the deal in internal discussions, while VP Vance and envoys Witkoff and Kushner supported it.

- Iran's Foreign Minister Araghchi said the formal activation of the MOU will be on Friday. That will immediately end the war, including in Lebanon. Second phase negotiations would then commence immediately. Next round of US-Iran talks will start Friday in Switzerland.

- Israeli artillery shelling was reported in the Nabatieh district of southern Lebanon. It was separately reported that Hezbollah fired rockets and artillery at Israeli soldiers, while the Israeli military said it intercepted numerous rockets launched by Hezbollah towards troops in southern Lebanon.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as the prior day's rally and US-Iran peace deal euphoria petered out amid a continued lack of concrete details regarding the interim agreement and as market participants turn their attention to this week's busy slate of central bank policy decisions. ASX 200 was led lower by weakness in tech, consumer discretionary and industrials, while participants also digested the RBA rate decision in which the central bank paused after three consecutive rate hikes, but warned of potential future hikes if necessary and remained hawkish regarding inflation. Hang Seng and Shanghai Comp were choppy as participants digested mixed activity data in which Industrial Production topped forecasts, but Retail Sales missed and printed in contraction territory, while the PBoC continued its increased liquidity efforts.

Top Asian News

- China's National Bureau of Statistics spokesperson said China's economic foundation needs to be strengthened, and that the external situation is complex and volatile, while China is to strengthen counter-cyclical adjustments, and will stabilise employment and the market. NBS also stated that China is to expand domestic demand and that some companies face relatively big pressure. Furthermore, the stats bureau spokesperson said there is still ample space for China to expand investment and that stronger employment and income growth are needed to boost consumption, as well as stated that China has ample policy space, reserves and flexible tools available to ensure stable economic growth, but also acknowledged that China's foreign trade faces some pressure due to external uncertainties.

European bourses (STOXX 600 +0.5%) are extending on Monday's gains but yet to reach the best levels reached in the prior session. To recap the main driver, the US and Iran have agreed to a preliminary deal to end the conflict and reopen the Strait of Hormuz. However, new updates regarding the deal have been light as markets now wait for the official MoU signing on Friday. European sectors are broadly higher. Industrial Goods & Services (+1.5%) and Banks (+1.2%) are the clear outperformers, with Media (+0.8%) completing the top 3 sectors. On the downside, Autos (-0.9%) and Retail (-0.6%) are the underperformers.

Top European News

- UK Chancellor Reeves said will see a further "big" uplift in defence spending within the DIP and hopes to get to the next budget without the need to raise taxes.

- Germany's RWI expects the German economy to stagnate in Q2 2026, sees inflation at 3.1% in 2026 and 2.9% in 2027, sees growth at 0.8% in 2026 and 2027.

- EU officials are drafting a blueprint to manage banking crisis liquidity, according to POLITICO.

FX

- DXY was firmer in APAC trade, though gains have reversed since as energy benchmarks continue lower on reports that Qatar is to reach 80% output within two months of the Strait of Hormuz reopening. As oil gradually returns to around pre-war levels, focus is ever-shifting towards central bank actions rather than terms of trade. On that note, Warsh’s first FOMC meeting as Chair is due on Wednesday, widely expected as a hold. The docket today is light, with just ADP employment weekly and Import/Export prices due. DXY marked a session low just above the 99.60 mark, currently unchanged on the day.

- RBA held the cash rate steady at 4.35% as expected, striking a hawkish tone by explicitly signalling further hikes on the table. Alongside the high bar set by markets of hawkishness by the RBA, participants this morning seemingly focused on the soft Australian growth story, with the Aussie under modest pressure, albeit just reversing some of Monday’s risk-on bid. Despite the reaction post-RBA, Westpac says next hike could come in August should the quarterly June inflation figure be strong, while ING suggests it is likely to remain on hold through year-end as inflation broadly tracks the board’s baseline scenario. AUD/USD -0.1% but within Monday's range. The pair marked a session low just above 0.7040.

- BoJ hiked rates by 25bps to 1.00% in a 7-1 vote split, as expected. Asada was the dissenter, arguing that downside risks to employment and production were larger than inflation risks. JPY unreactive to the meeting/presser with Uchida not providing a clear bias, as had been expected heading into the presser given he was standing in for Governor Ueda. Not many clues as to what future policy will look like, with market pricing unchanged, with 85% probability of the BoJ’s next tightening in December. USD/JPY U/C, was supported by 160.00 throughout the meeting/presser.

Central Banks

- The BoJ hiked its short-term interest rates by 25bps to 1.00%, as expected, while it pauses tapering of bond buys in which it will keep monthly pace of JGB buying at around JPY 2tln from April 2027. Decision made by 7-1 vote, with Asada dissenting against a hike.

- In the post-policy press conference, BoJ's Uchida said financial conditions have been accommodative while stating there is a risk of underlying inflation deviating upward to a level above the price target. All-in-all, Uchida avoided any commentary pertaining to forward guidance.

- The RBA kept the Cash Rate unchanged at 4.35%, as expected, but warned of potential further hikes if necessary citing persistent inflation and oil supply disruptions.

- In the post-policy press conference, RBA Governor Bullock said inflation remains too high, with the Board still concerned about inflation. No hike was considered at the meeting but doesn't rule out that the Bank might have to do more on rates. Risks are still to the upside.

Fixed Income

- Global fixed benchmarks (ex-JGBs) started the European session trading on either side of the unchanged mark, with the complex ultimately taking a breather from the gains seen in the prior session. However, some pressure was seen in the crude complex soon after the European cash open, which helped lift fixed paper to highs. As such, yields are lower across the curve, but with underperformance now in the belly of the curve, in contrast to short-end underperformance seen on Monday; nonetheless, the bull-steepening bias remains. The slight pressure in the belly is perhaps indicative of markets beginning to price in the economic impact of the resumption of flows through the Strait of Hormuz; recent updates out of Qatar have suggested that it can restore half of its LNG output within a month, 80% within two months

- JGBs (-47 ticks) lag vs peers, given the BoJ’s decision to hike rates by 25bps (as expected) and its announcement to pause the tapering of JGB purchases from FY27. The accompanying presser provided little updates, with Deputy Governor Uchida avoiding any commentary pertaining to forward guidance. As it stands, markets assign an 85% chance of a hike by year-end, so focus remains firmly on Ueda’s comments when he returns from hospital.

- USTs (+6 ticks) trade at the upper end of a 109-19 to 109-26+ range. Overnight action saw the benchmark move sideways around the unchanged mark, before then moving higher as energy prices fell. From a yield perspective, the US 10yr remains just shy of the 4.50% mark, last at 4.44% - and well beyond pre-war levels at c. 4.00%. Economists will argue that, for now, the damage to the global economy has already filtered through; the US is dealing with elevated inflation, which may keep yields propped up in the short-term.

- Bunds (+17 ticks) and Gilts (+30 ticks) follow the bullish bias mentioned earlier, and trade towards their respective highs. The former digested a better than expected ZEW survey, as markets saw more positive developments on the US-Iran situation. Elsewhere, a 2036 Gilt auction passed with solid demand.

- Germany sells EUR 3.824bln vs exp. EUR 5bln 2.50% 2031 Bobl: b/c 1.64x (prev. 1.32x), average yield 2.64% (prev. 2.85%), retention 23.5% (prev. 23.12%).

- The UK sells GBP 4.25bln 4.875% 2036 Treasury Gilt: b/c 3.46x (prev. 3.45x), average yield 4.858% (prev. 5.026%), tail 0.1bps (prev. 0.3bps).

Commodities

- Geopolitical newsflow has calmed down as markets now await the official MoU signing on Friday. More recently, Iranian Foreign Minister Araghchi said a new round of US-Iran talks will start on the day of the signing in Switzerland. Concrete MoU details remain unclear. Overnight, US President Trump said Iran has agreed never to have a nuclear weapon.

- Crude futures traded rangebound throughout the Asia-Pac session but have seen pressure in recent trade, driven by reports that Qatar is planning to rapidly boost LNG production to about 50% capacity a month after safe passage through the Strait is restored and c. 80% within two months. WTI Jul'26 slips below the USD 80/bbl mark, trading at the lower end of its USD 78.41-81.58/bbl range. Brent Aug'26 kissed the round USD 81/bbl mark (USD 81.00-83.80/bbl). Dutch TTF also lower, but remains above the EUR 42/MWh mark.

- Spot gold is on a firmer footing, after gains were pared back slightly in the latter end of Monday's session. The yellow metal remains above the key USD 4300/oz handle, currently trading at the upper end of its USD 4306-4336/oz band. According to a WGC survey of 74 central banks, 45% said they plan to buy gold in the coming year, with only 1 saying it plans to cut its holdings. “I think the fall in the price is an opportunity for some central banks to start buying in,” said Shaokai Fan, global head of central banks for the WGC.

- 3M LME Copper trades choppy, with initial weakness driven by the disappointing Chinese domestic data. Retail sales fell for the first time in over 3 years, contracting 0.6% in May and missing estimates of 0%. In contrast, industrial production rose 4.5%, beating the 4.3% consensus. The red metal trades in the bottom half of its USD 13.64k-13.77k/t range.

- Qatar to restore half of its LNG output a month after the Strait of Hormuz opens, with output to reach 80% of full output within two months, according to Bloomberg.

- Iranian Oil Minister announced plans to rapidly increase gas production in fields covered by the Central Iranian Oil Company.

- Iranian Energy Minister said Tehran will soon connect its electricity grid with Qatar.

- Mitsui OSK Lines (9104 JT) CEO said that many operators would wait at least a couple of weeks or a month before resuming normal transit through the Strait of Hormuz.

- Goldman Sachs lowered its Q4'26 Brent crude forecast to USD 80/bbl (prev. USD 90/bbl). Cut 2027 Brent forecast to USD 75/bbl (prev. USD 80/bbl), cut WTI forecast to USD 75/bbl in Q4'26 and USD 70 for 2027.

US Event Calendar

- 8:30 am: May Import Price Index MoM, est. 1%, prior 1.9%

- 8:30 am: May Housing Starts, est. 1430k, prior 1465k

- 8:30 am: May Building Permits, est. 1417.5k, prior 1423k

DB's Jim Reid concludes the overnight wrap

Markets have had an eventful 24 hours, with a major rally in the US and Europe as investors reacted to the US-Iran deal announced over the weekend. So that’s driven a wave of optimism across multiple asset classes, with Brent crude (-4.76%) closing at a three-month low of $83.17/bbl, along with a further -0.23% decline this morning to $82.98/bbl. And with investors pricing out the chance of stagflation, the S&P 500 (+1.65%) closed back within 1% of its record high, whilst the STOXX 600 (+0.19%) closed at its first record since the conflict began.

Overnight, there’s been no letup in the newsflow, as the Bank of Japan delivered a 25bp rate hike as expected, taking their policy rate to its highest since 1995, at 1%. They also signalled further hikes to come, and their statement said that “given that underlying CPI inflation has been approaching 2 percent and financial conditions have been accommodative, the Bank will continue to raise the policy interest rate”. Moreover, they also announced they’d stop tapering their monthly JGB purchases in the months ahead. So at the moment, they’re still purchasing 2.7tn yen per month, and the plan is to keep reducing those monthly purchases by 200bn yen each quarter until Q1 2027. But then from April 2027, they’re going to keep that pace steady at around 2tn yen. In response, Japanese government bonds have seen a decent selloff, with the 10yr yield up +7.5bps to 2.64%, but the Nikkei (+0.42%) is still on track for another record.

Speaking of central banks, the Reserve Bank of Australia also announced they’d leave rates unchanged this morning. The move was widely expected, and keeps their cash rate at 4.35% after hiking at the last 3 meetings. However, even as they held rates for the first time this year, the statement also explicitly suggested they might hike again if needed, whilst warning that “ headline and underlying inflation are still too high.” Against that backdrop, yields on 10yr Australian government bonds are up +3.5bps this morning at 4.84%.

Elsewhere overnight, China’s activity data for May was released, which showed retail sales down by -0.6% on a year-on-year basis (vs. -0.2% expected). Meanwhile, fixed asset investment over the first five months of the year was also down -4.1% compared to the previous year (vs. -2.3% expected). That said, there were some upside surprises, with industrial production up +4.5% year-on-year in May (vs. +4.4% expected). Meanwhile, equities in mainland China have seen modest gains, with the CSI 300 (+0.13%) and the Shanghai Comp (+0.06%) both up slightly.

More broadly, markets have clearly stabilised this morning after the surge of optimism that surrounded the deal yesterday. So futures on the S&P 500 (-0.08%) are pointing slightly lower, and the 10yr Treasury yield is up +0.2bps at 4.48%. In part, that comes as there’s still a lot of question marks over how the deal will be implemented, as we don’t have the full details or a text yet. Nevertheless, we did hear from a US official yesterday, who briefed reporters on the Memorandum of Understanding (MoU). They said the details would be released in 24-48 hours, and it would provide for an immediate opening of the Strait of Hormuz, although it would take time given the mines. Meanwhile, the US and Iran would launch technical talks later this week. Then later on CNN, Vice President JD Vance said the MoU was a “very general” document and “about a page and a half”.

As mentioned, the deal’s announcement led to a clear fall in oil prices, with Brent crude at a three-month low. But we also saw the futures curve increasingly normalise, as longer-dated futures moved more in line with the front-end price. So the 6-month future came down -3.45% to $78.87/bbl, meaning that the difference between the 6-month and the front-end future was actually the smallest since the conflict began, at just $4.30. In other words, investors are no longer pricing a sharp fall in oil prices over the next six months, as that was predicated on an agreement that’s now been announced. Moreover, the decline was clear across other energy commodities, with European natural gas futures (-9.12%) closing at a 7-week low of €42.51/MWh.

With energy prices coming down, that helped to ease fears about inflation on both sides of the Atlantic. For instance, the 1yr Euro inflation swap (-12.0bps) fell to just 2.713%, whilst the 1yr US inflation swap (-8.8bps) fell to 2.663%, which for both was the lowest in three months. In addition, investors also moved to price out the chance of aggressive rate hikes, with a more dovish profile for central banks over the months ahead. So for the Fed, investors were only pricing in a 79% chance of a rate hike by the December meeting. And over at the ECB, investors were pricing in just 31.4bps of further hikes by December, implying growing doubt about a third ECB hike this year, given they already delivered a 25bp hike last week.

With inflation fears easing and rate hikes being priced out, that led to a sovereign bond rally on both sides of the Atlantic. So in the US, the 2yr Treasury yield (-1.5bps) fell to 4.066%, whilst the 10yr Treasury yield (-0.6bps) fell to 4.47%. Meanwhile in Europe, there were even bigger declines given their relative exposure to the energy shock, with yields on 10yr bunds (-4.1bps), OATs (-4.8bps) and BTPs (-5.3bps) all falling back.

That backdrop was a very strong one for equities too, with a decent surge across the board. For instance, the S&P 500 (+1.65%) closed less than 1% beneath its record high, and there were even bigger gains for tech stocks, with the NASDAQ (+3.07%) surging. Notably, the Philly semiconductor index (+5.45%) even closed at a record high, which felt a long way from a week-and-a-half ago, back when the index slumped more than -10% on the day of the jobs report that led markets to price in a more hawkish Fed. Then in Europe, the STOXX 600 (+0.19%) finally closed at a new record for the first time since February 27, the day before the Iran conflict began.

Finally, there wasn’t much data yesterday, although a few of the US releases came in on the softer side. So industrial production was only up +0.1% in May (vs. +0.3% expected), albeit with a two-tenths positive revision to the April reading. Then the Empire State manufacturing survey fell more than expected to 5.7 (vs. 13.7 expected), whilst the NAHB’s housing market for June unexpectedly fell to 35 (vs. 37 expected).

Looking at the day ahead now, data releases include the German ZEW survey for June, and US housing starts for May. Otherwise, central bank speakers include the ECB’s Escriva, Lane and Sleijpen.

Ayrıca Şunları da Beğenebilirsiniz

BitGo Launches Stablecoin Minting and Redemption Service for Institutions

Hedera Price Prediction Holds Bullish as Iran Peace Deal Pushes Bitcoin Above $65,000 and Pepeto Presale Passes $10 Million

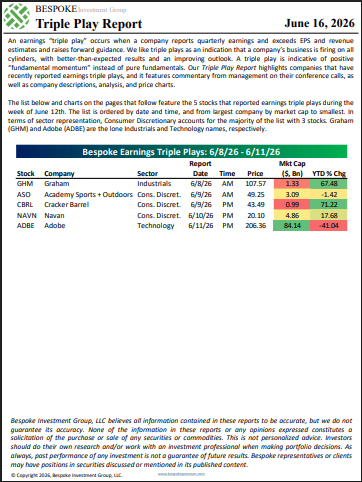

The Triple Play Report: 6/16/26

Popüler Haberler

Daha fazla