Meta Price Prediction: The Case for 30%+ Upside After a Selloff

The post Meta Price Prediction: The Case for 30%+ Upside After a Selloff appeared first on 24/7 Wall St..

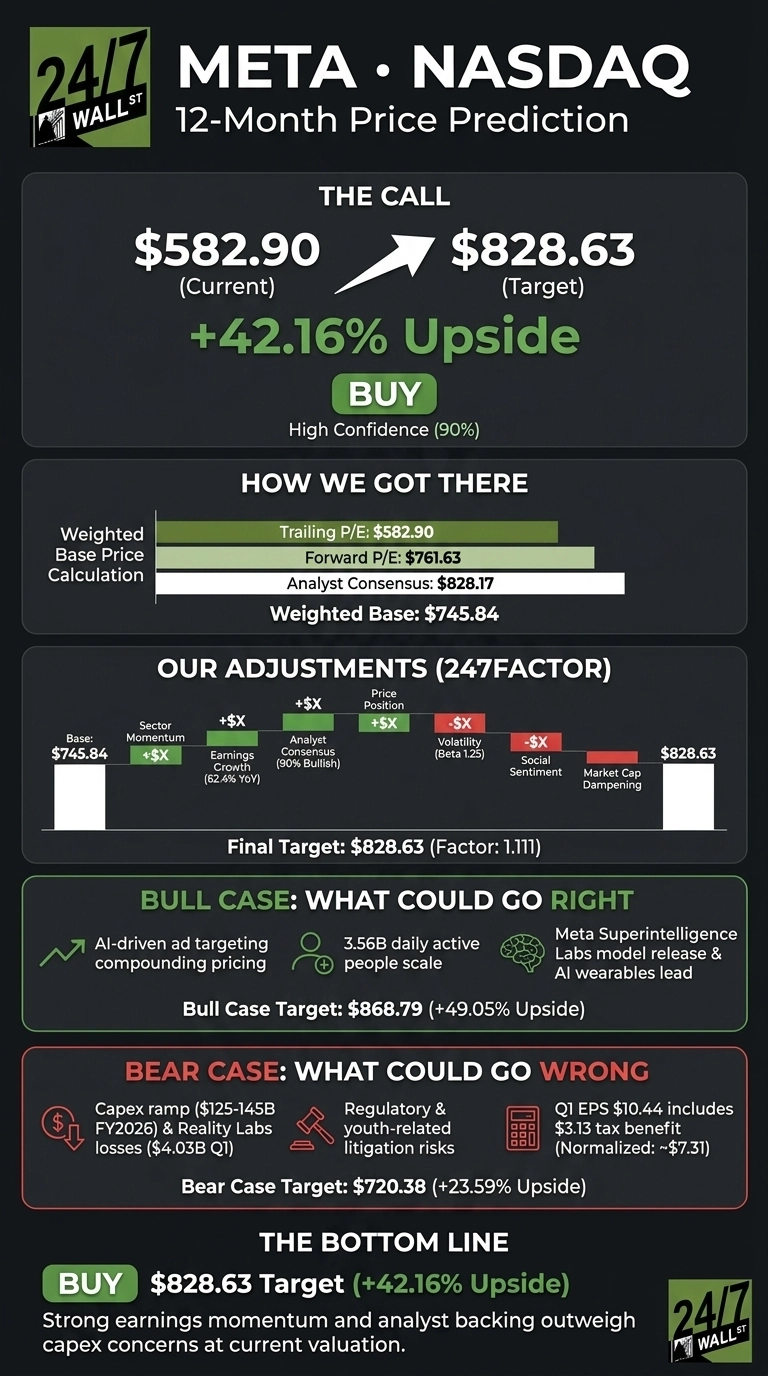

Meta Platforms (NASDAQ:META) has been through the wringer. The stock is down 18.05% over the past year and 11.54% year to date, with a brutal 4.9% single-day drop on July 2, 2026. After running the numbers, the selloff looks overextended relative to fundamentals.

Our 24/7 Wall St. price target for Meta is $828.63, implying 42.16% upside from $582.90. The recommendation is buy, with high confidence at 90%.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $582.90 |

| 24/7 Wall St. Price Target | $828.63 |

| Upside | 42.16% |

| Recommendation | BUY |

| Confidence Level | 90% |

How a $1.28 Trillion Giant Fell Out of Favor

Meta peaked near $785.23 in August 2025 before grinding lower into July 2026. The catalysts for the pullback were largely self-inflicted: management raised FY2026 capex guidance to $125-145 billion, up from the prior $115-135 billion range, citing higher component pricing and data center costs. Reality Labs is still bleeding, with a $4.03 billion operating loss in Q1 2026.

Yet the underlying business is roaring. Q1 2026 revenue jumped 33.1% YoY to $56.31 billion, ad impressions rose 19%, and price per ad climbed 12%. That is Meta’s fifth consecutive EPS beat. Reddit captured the mood best with a viral wallstreetbets post about “Suckerberg panic bought the entire AI chip supply,” which drew 13,591 upvotes.

The Case for $868 and Higher

The bull scenario projects $868.79, or 49.05% upside. The core drivers: Meta Superintelligence Labs released its first model in Q1, 3.56 billion daily active people across the Family of Apps, and AI-driven ad targeting that is compounding pricing power.

Ray-Ban Meta glasses give Meta the early lead in AI wearables. Of 63 analysts covering the stock, 57 rate it Buy or Strong Buy with zero sells. The forward P/E sits at just 19, a modest multiple for a business compounding earnings at this rate.

What Could Go Wrong

The bear case targets $720.38, still 23.59% above spot. Risks are real: FY2025 free cash flow fell 19.39% as capex nearly doubled, youth-related litigation trials are scheduled through 2026, and Q1’s $10.44 EPS was flattered by a $3.13 per share tax benefit from Treasury Notice 2026-7. Normalized operating EPS was closer to $7.31.

Bulls would counter that the capex ramp is building the AI infrastructure that already powered 33.1% Q1 revenue growth. Operating income still rose 30.29% YoY, and the balance sheet remains fortress-grade with interest coverage of 71x.

Meta Price Prediction 2026-2030

The 24/7 Wall St. price target of $828.63 reflects a rare setup: a mega-cap with 42.16% modeled upside, 90% confidence, and a Street that is uniformly constructive. The tie-breaker is valuation.

A 19 forward P/E on a business growing revenue at 33.1% is asymmetric. The setup strengthens if Q2 revenue lands at the high end of the $58-61 billion guide. Risks intensify if Reality Labs losses balloon or capex guidance climbs again.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $828.63 |

| 2027 | $975 |

| 2028 | $1,140 |

| 2029 | $1,335 |

| 2030 | $1,549.79 |

These projections assume Meta continues executing on AI monetization and family of apps growth. Significant upside could come from Reality Labs turning profitable; downside risk hinges on regulatory outcomes and capex discipline.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Meta didn’t make the cut. Grab the names FREE today.

The post Meta Price Prediction: The Case for 30%+ Upside After a Selloff appeared first on 24/7 Wall St..

Ayrıca Şunları da Beğenebilirsiniz

Critical USDT0 Response to Drift Hack Exposes Stark Contrast in Stablecoin Security Protocols

Bitcoin Exchange Bull Bitcoin Asks France’s Highest Court to Block EU Crypto Tax Rule

AT&T leaves rivals flat-footed as bankrupt carrier folds

Popüler Haberler

Daha fazla