Palo Alto Networks Just Got a Street-High $420 Target. Here’s Where the Stock Could Go

Key Stats for Palo Alto Networks Stock

- Current Price: $345.55

- Target Price (Mid): ~$475

- Potential Total Return: ~37%

- Annualized IRR: ~8% / year

- Earnings Reaction: (5.64%)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Palo Alto Networks (PANW) has a problem that most companies would envy. The stock keeps making new records, and Wall Street keeps chasing it higher. On July 1, Wells Fargo analyst Michael Turrin raised his price target to a Street-high $420 from $325, kept an Overweight rating, and added the stock to the firm’s third-quarter tactical ideas list. PANW jumped more than 3% that day and pushed to a fresh 52-week high, with TIKR data showing a high of $358.10 over the past year.

That upgrade did not arrive alone. BTIG analyst Gray Powell lifted his target to $380 from $333 the same day and called PANW his top pick across cybersecurity coverage. Both moves followed a record fiscal Q3 that turned the AI-threat narrative into hard numbers. The stock trades around $345 today, up roughly 22% over the trailing five days heading into the July highs, and now sits near 88x forward earnings.

So the question is not whether the business is executing. It is. The question is whether the Street’s enthusiasm has run ahead of what the math will actually pay you from here. The bulls see the most important demand cycle in the company’s history. The skeptics see a premium multiple with insiders selling into the rally. Both cannot be fully right.

Why Wall Street Keeps Raising Targets

The catalyst is straightforward. Wells Fargo said it expects the debate over organic versus acquired growth to fade once Palo Alto shifts to new segment-level reporting in fiscal 2027, a change it reads as a sign of strength rather than obfuscation. That reporting shift matters because it removes the one line of attack skeptics have leaned on since the CyberArk deal closed.

The fundamentals behind the upgrades are real. In fiscal Q3 2026, reported June 2, revenue grew 31% year-over-year to $3.0 billion, and adjusted earnings of $0.85 beat the top end of guidance by $0.05. Next-generation security ARR (NGS ARR), meaning the annualized value of the company’s recurring subscription products, reached $8.13 billion, up 60%. Management raised full-year guidance across every metric.

The demand story rests on a specific claim from the top. CEO Nikesh Arora argued that frontier AI has collapsed the timeline of an attack. “When weaponized by adversaries, these frontier models can identify and weaponize vulnerabilities in mere minutes, a process that previously required months of manual effort,” he told analysts. That matters because it reframes cybersecurity budgets from discretionary to urgent, and Arora went further, telling the Street that Anthropic’s Mythos model has “increased the terminal value of the entire cybersecurity industry.” Terminal value is the long-run worth of a business, and lifting it is exactly what justifies a higher multiple.

The proof points backed the rhetoric. Prisma AIRS, the company’s AI security platform, tripled its customer count in a single quarter to over 300, and management sees a clear path to $100 million in ARR for a product that did not exist a year ago. Next-generation firewall bookings rose nearly 40%, the strongest hardware quarter in a decade, as AI data centers emerged as a new class of buyer. XSIAM, the AI-driven security operations platform, crossed $600 million in ARR, doubling year-over-year.

Palo Alto Networks Subscription, Product, & Support Operating Revenue (TIKR)

Palo Alto Networks Subscription, Product, & Support Operating Revenue (TIKR)

See historical and forward estimates for Palo Alto Networks stock (It’s free!) >>>

The Valuation Math Wall Street Is Waving Through

Here is where a second opinion earns its keep. PANW trades at roughly 88x NTM P/E and 56.84x NTM EV/EBITDA. Enterprise value to revenue sits at 21.16x on a forward basis. Those are numbers that leave no room for a stumble.

Peer context sharpens the point. Among software names on the TIKR Competitors page, CrowdStrike (CRWD) trades even richer at 31.02x NTM EV/revenue and 102.44x NTM EV/EBITDA, while Fortinet (FTNT), the more mature network-security rival, sits at a far cooler 13.99x revenue and 38.54x EBITDA. Palo Alto lands between the two, priced like a high-growth compounder rather than the firewall business it used to be. The premium to Fortinet is defensible given Palo Alto’s 60% ARR growth and broader platform, but the discount to CrowdStrike tells you the market still prices more future upside into CRWD. That is the tension that the multiple cannot resolve on its own.

It is also worth noting where consensus is heading. The TIKR snapshot pegs the Street’s average target near $318, but that figure is already being overtaken: the three most recent analyst actions cluster around $380 to $420, so the average is climbing week by week as the sell side catches up to the rally.

The GAAP picture is the other caution. Palo Alto reported a net loss of $0.22 per share for the quarter, driven by acquisition and integration costs tied to CyberArk and Chronosphere. Non-GAAP EPS was healthy at $0.85, but the gap between the two figures is where integration risk lives. Stock-based compensation rose to 17% of revenue, which CFO Dipak Golechha expects to return to pre-acquisition levels within 12 to 18 months. Free cash flow, the cash a business generates after capital spending, tells a more reassuring story: adjusted free cash flow reached $910 million in the quarter, up 57%, and the trailing-twelve-month margin hit 38.5%.

The bigger structural question is whether the demand Arora describes converts on his timeline rather than a slower one. Management is guiding to a 40% free cash flow margin in fiscal 2028 and says it is now three to six months ahead of schedule on converging CyberArk’s profitability with its own. If that holds, the premium compresses gracefully as earnings catch up. If integration slips or organic growth decelerates once the acquired contribution stops being broken out, the skeptics get their first real evidence that the market paid too much.

Palo Alto Networks NTM (P/E) & NTM EV/EBITDA (TIKR)

Palo Alto Networks NTM (P/E) & NTM EV/EBITDA (TIKR)

See how Palo Alto Networks performs against its peers in TIKR (It’s free!) >>>

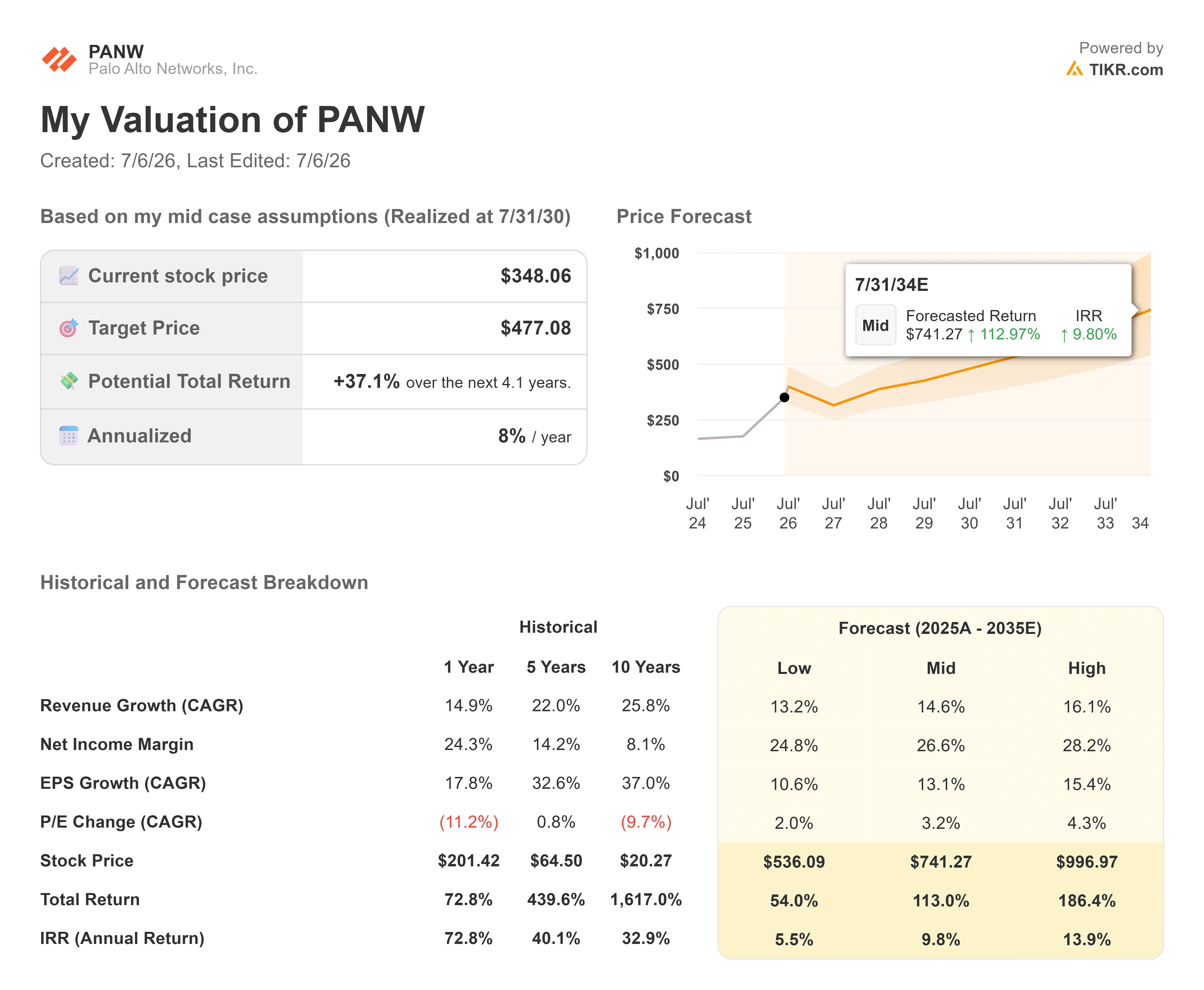

TIKR Advanced Model Analysis

- Current Price: $348.06

- Target Price (Mid): ~$475

- Potential Total Return: ~37%

- Annualized IRR: ~8% / year

Palo Alto Networks Advanced Valuation Model (TIKR)

Palo Alto Networks Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Palo Alto Networks stock (It’s free!) >>>

Using the mid-case, the TIKR model points to a target of around $475, an implied total return of roughly 37%, and an annualized return of about 8% per year. Notably, that mid-case target sits above the Street’s current average, yet the annualized return is only modest, because the starting multiple is so high that most of the gain is spread across several years.

Two revenue drivers anchor the case. The first is platformization, where customers consolidate spending onto Palo Alto’s network, cloud, and security-operations platforms, lifting revenue per account. The second is AI-security attach, led by Prisma AIRS and XSIAM, which opens entirely new subscription lines as enterprises move AI workloads into production. The margin driver is the shift toward recurring software, which now makes up 46% of trailing product revenue versus 22% three years ago. The primary risk is multiple compression: at 88x forward earnings, even strong execution can produce mediocre returns if the P/E normalizes faster than earnings grow.

The upside: if AI-driven demand pushes revenue growth toward the high-case 16% CAGR with margins expanding past 27%, the model’s high scenario points to returns near 14% annually.

The downside: if growth settles nearer the low-case 13% and the multiple compresses, the annualized return falls toward the low single digits.

Conclusion

The signal to watch is the fiscal Q4 report on August 17. Good looks like NGS ARR landing at or above the $8.9 billion guide with the fiscal 2028 free cash flow margin target reaffirmed, which would validate the Street’s march toward $420. Bad looks like organic growth decelerating just as the company stops breaking out the acquired contribution, the exact seam skeptics have been probing. Wells Fargo is betting the reporting change signals confidence. August is when management has to prove it. At 88x forward earnings, the record high bought Palo Alto a very high bar to clear.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Palo Alto Networks?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Palo Alto Networks, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Palo Alto Networks alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Palo Alto Networks on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Forget Software: The COPX ETF Is the Pick-and-Shovel AI Trade Hiding in Plain Sight

Dow Jones Industrial Average Flirts With Historic Milestone Before Pulling Back

Was Michael Burry Right About Palantir? PLTR Is Still Down Over the Past Year