Broadcom Stock: Is the Google Chip-Share Fear Overblown in 2026?

Key Stats for Broadcom Stock

- Current Price: $360.45

- Target Price (Mid): ~$1,000

- Street Target: ~$525

- Potential Total Return: ~177%

- Annualized IRR: ~26% / year

- Earnings Reaction: -12.59% (June 3, 2026)

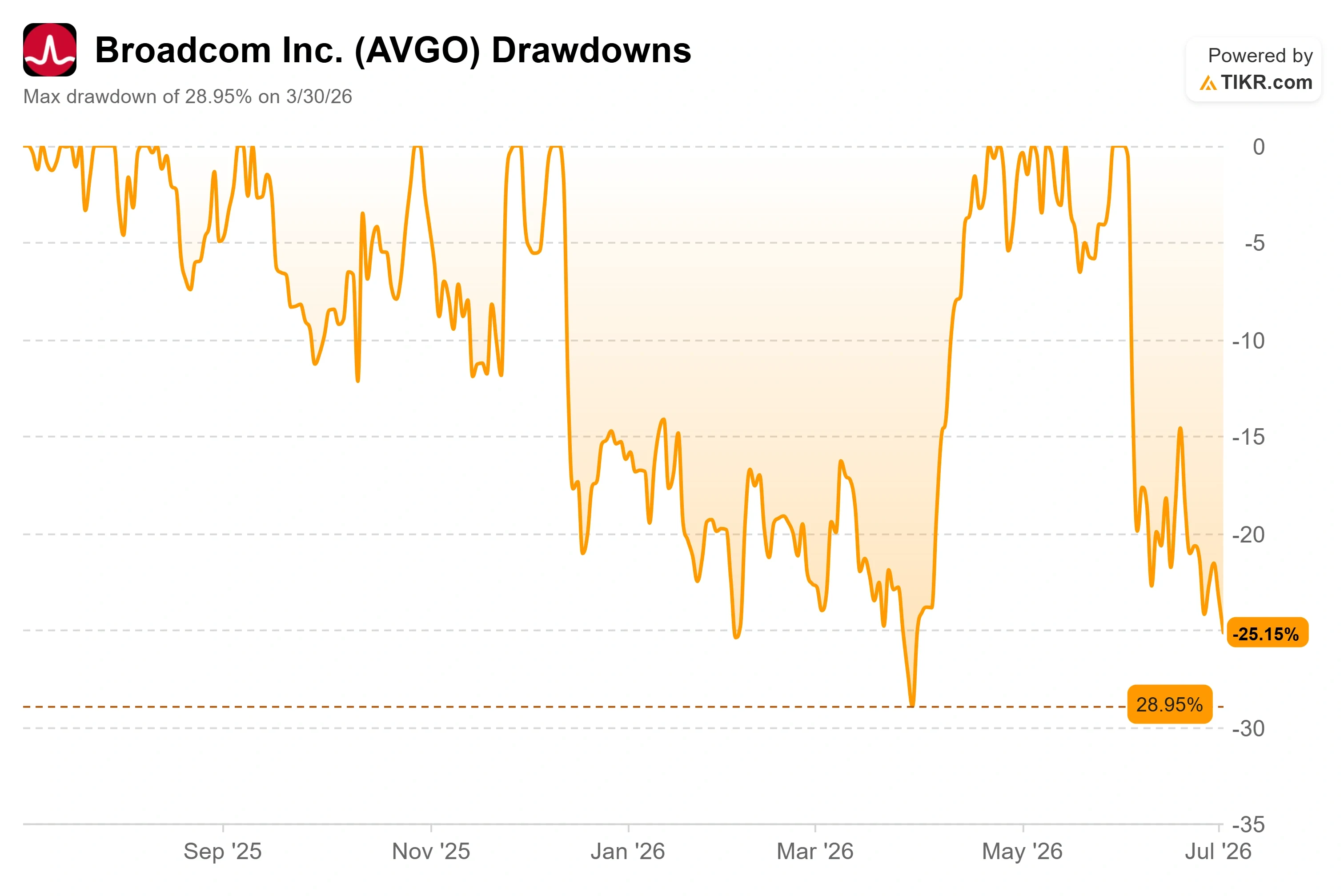

- Max Drawdown: -28.95% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Broadcom Inc. (AVGO) has become the stock the AI trade cannot agree on. It just posted the best quarter in its history, and it is down about 25% from its 2026 high anyway. The reason is not the numbers management reported. It is a fear about what one customer might do next.

That fear got a name on June 3, when Macquarie cut Broadcom to Neutral from Outperform and dropped its price target to $437. The firm’s logic was specific and unsettling: it expects Broadcom’s share of Google’s custom-chip revenue to fall from roughly 95% in 2026 to 80% in 2027 and 65% by 2028, as MediaTek takes a larger role and Google leans harder into its own silicon. For a company whose whole bull case rests on being the indispensable partner to hyperscalers, that is the one downgrade that lands.

Why one downgrade moved a $1.7 trillion stock

The trigger is real. In June, multiple reports indicated MediaTek had secured the contract to help build an enhanced version of Google’s next-generation TPU, the tensor processing unit that runs Google’s AI workloads. The variant, reportedly codenamed Triggerfish, is said to carry two to three times the on-chip memory of its predecessor. Broadcom still designs the higher-margin training version, but a second design house in the room changes the leverage. Macquarie read that shift and downgraded on it.

The market had already been nervous. Broadcom peaked at a closing high near $481 in early June and now trades at $360.45, a drop of about 25%. On June 3, the earnings reaction sent the stock down 12.59%, the steepest of its last five earnings reactions. The business grew fast. The stock still got hit. That gap between execution and price is the whole story right now.

Not everyone agrees with the bear read. JPMorgan reiterated an Overweight rating with a $580 target and said it would be an aggressive buyer at current levels. The firm’s research indicates the Google TPU v9 program with Broadcom has not been delayed or canceled, contrary to what it called noise from sell-side desks and the Asia supply chain. So the debate is not soft. One side sees a share loss beginning. The other sees a durable moat being mispriced.

Broadcom Drawdowns (TIKR)

Broadcom Drawdowns (TIKR)

See historical and forward estimates for Broadcom stock (It’s free!) >>>

What the Q2 Call actually said about Google

The most useful voice in this argument is the one the downgrade talks around. On the Q2 call, an analyst asked CEO Hock Tan directly about share within the Google relationship. Tan did not dodge the diversification question. He acknowledged it, then reframed the stakes.

CEO Hock Tan was direct about the strength of the agreement. “It’s a commitment that is very substantial in dollars. Very, very substantial amount of dollars,” he said, before adding that Broadcom fully expects “some diversity of sources” for Google, given how fast the customer’s own AI consumption is growing. That matters because it tells investors the base case already includes MediaTek. Broadcom is not being surprised by share dilution. It priced it in and still signed a very large commitment.

The bookings number makes the same point from the other direction. Tan said AI semiconductor bookings topped $30 billion in the quarter against just $10.8 billion shipped. He described demand across the customer base as “insatiable,” and said the company now has revenue visibility running all the way to 2028, up from 2027, just three months earlier. A company losing its grip on the AI cycle does not book three times what it ships and extend its visibility by a full year.

The customer base is widening, not narrowing

The subtler flaw in the pure share-loss thesis is that it treats Google as the whole story. It is not anymore. Broadcom guided full-year 2026 AI semiconductor revenue to $56 billion, up roughly 180% from fiscal 2025, and reaffirmed a target above $100 billion for fiscal 2027. That growth is spread across six core custom-silicon customers, not one.

Tan walked through the roster on the call. Anthropic is set to access more than 1 gigawatt of Broadcom TPU-based compute in 2026 and signed on for another 5 gigawatts starting in 2027. OpenAI has a contractual commitment to deploy 1.3 gigawatts in 2027 as part of a larger 10-gigawatt agreement. Meta signed for multiple generations of its MTIA accelerator, the Meta Training and Inference Accelerator, with an initial 1-gigawatt order already received. If Google’s mix inside that pool shrinks while the pool itself doubles, Broadcom can lose share and still grow revenue sharply. That is the arithmetic the downgrade leaves out.

Margins are the one place bears have a cleaner point. Consolidated gross margin is guided down to about 74% in Q3 as lower-margin custom chips grow faster than high-margin software. But that is mix, not decay. CEO Hock Tan was explicit that structural semiconductor margins remain stable, and CFO Kirsten Spears noted that the AI networking side carries rich margins that offset the custom-silicon dilution. Operating margin is still guided to hold near 67%, flat quarter over quarter, on the strength of Broadcom’s operating leverage.

Against its peers, the valuation reads less like a premium and more like a stock that has not recovered. Broadcom trades at an NTM P/E, the next twelve months price-to-earnings multiple, of about 23x. NVIDIA sits near 20x and AMD near 59x, while custom-silicon rival Marvell trades above 54x. Broadcom is not the cheapest name in AI chips, but it holds some of the most durable multi-year contracts in the group and trades well below the peer average. That looks more like an unfinished post-earnings reset than a market pricing in permanent decline.

Broadcom Street Targets (TIKR)

Broadcom Street Targets (TIKR)

See how Broadcom performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $360.45

- Target Price (Mid): ~$1,000

- Potential Total Return: ~177%

- Annualized IRR: ~26% / year

Broadcom Advanced Valuation Model (TIKR)

Broadcom Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Broadcom stock (It’s free!) >>>

TIKR’s mid-case model values Broadcom at around $1,000 by October 2030. From the current price, that implies a potential total return of around 177%, or roughly 26% annualized over the next 4.3 years.

The two revenue drivers behind that target are AI semiconductor scaling, where management guides revenue to double in the second half of fiscal 2026 and exceed $100 billion in fiscal 2027, and the VMware software base, where annual recurring revenue grew 17% year over year. The margin driver is mix and operating leverage: software gross margins above 93% offset lower custom-silicon margins, letting operating margin hold near 67% even as chip revenue climbs. The primary risk is the one Macquarie flagged: if hyperscaler insourcing accelerates faster than the customer pool expands, both share and pricing power compress at once.

The upside is that Broadcom converts its $30 billion booking quarter and 2028 visibility into shipped revenue while multiples normalize, and the stock re-rates toward the model target.

The downside is that Google’s diversification spreads to other customers, growth normalizes early, and the stock stays stuck near its reset multiple.

Conclusion

The next real test is the fiscal Q3 report, due September 2, 2026. The number that settles this debate is AI semiconductor revenue, guided to $16 billion. Hit or beat that, with reaffirmed or raised 2027 AI guidance above $100 billion, and the share-loss fear looks premature. Come in soft, or trim the AI outlook, and Macquarie’s thesis gets its first piece of evidence. Watch the bookings figure just as closely as the headline: another quarter of orders far above shipments would tell you demand still outruns any single customer’s diversification. Until then, this is a fight between a downgrade and a backlog, and the backlog is winning.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Broadcom?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Broadcom, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Broadcom alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Broadcom on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Forget Software: The COPX ETF Is the Pick-and-Shovel AI Trade Hiding in Plain Sight

Dow Jones Industrial Average Flirts With Historic Milestone Before Pulling Back

Was Michael Burry Right About Palantir? PLTR Is Still Down Over the Past Year